Recently released US January employment data showed that the resilience of the US economy continues after growing 2.5% in 2023.1 The Federal Reserve (Fed) insists that it is premature to expect ‘imminent’ rate cuts and as a consequence, the market has adjusted expectations. The current focus for markets continues to be on the 2023 4th quarter earnings season, with US numbers more positive than Europe. The Commercial Team at Santander Asset Management digs deeper in this week’s State of Play.

1. The US economy remains resilient

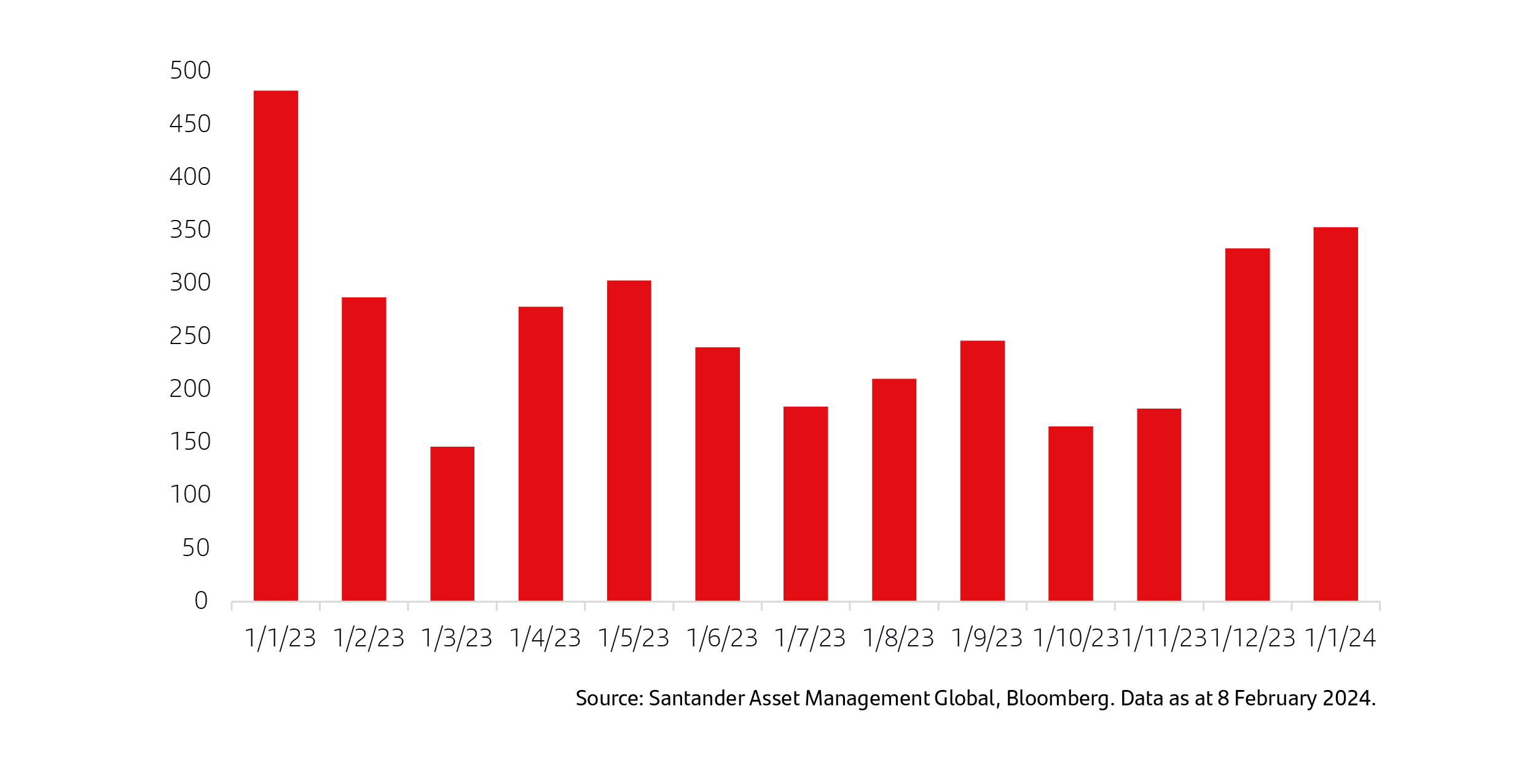

After surprising the market with +2.5% US GDP growth in 20231, far exceeding forecasts, the first data for 2024 confirmed that the economy remains resilient. In January, payrolls were 353,0002 , almost double what the consensus had expected, and the estimated data from previous months was also revised upwards.2 This sweet spot in the labour market can be explained in large part by the trajectory that consumer expenditure has, which gives some confidence that a favourable pace will be maintained in the coming months. The data has been accompanied by a higher-than-expected increase in average hourly earnings (+0.6% month on month)2, although the Fed benchmark on wages, the employment cost index, has been slowing since March 2022.3

US: Monthly nonfarm payrolls (thousands)

Nonfarm payroll measures the number of workers in the U.S. except those in farming, private households, proprietors, non-profit employees, and active military.

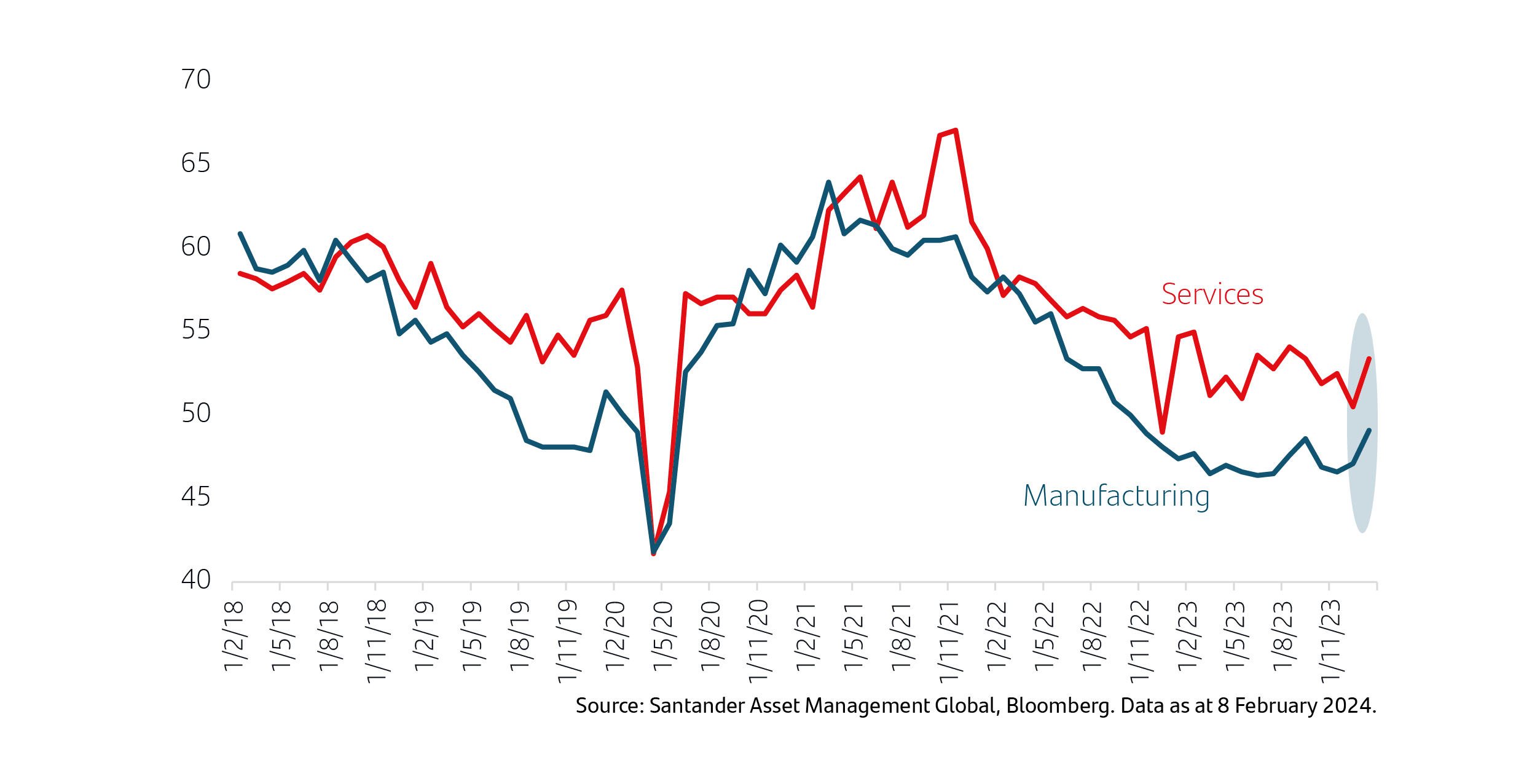

The other source of positive surprise has been the Institute for Supply Management (ISM) business confidence indicators. The index measuring the manufacturing sector, while still below the level of economic expansion of 50, rose in January to the highest level since October 2022.4 The corresponding index measuring services recorded a significant increase in January, reaching 53.4.4 While the expectation is that economic growth will continue in the US, the pace of such growth is likely to be slower than 2023 levels.

US: Institute for Supply Management (ISM) Manufacturing & Services measures

2. Central bank messaging and employment data changes rate cuts expectations

US employment data has clearly had an impact on what the market is expecting in terms of the schedule of upcoming rate cuts. Since the beginning of the year, the guidance from the Fed and the European Central Bank (ECB) has clearly been aimed at curbing investors’ expectations on when rate cuts will start.

To summarise Jerome Powell’s (Chair of the Federal Reserve) statements at the Fed’s most recent press conference: In order for the Fed to lower rates, they want to have more confidence in the inflation data and that lower inflation is sustainable. However, it is unlikely to have this certainty ahead of the next meeting in March.5

The strength of employment in January has reinforced this view and accentuated the update of market expectations for the Fed and also for the ECB, whose signals have also been in the same vein. Thus, the month of June has become the date with the full probability of the start of easing in the US and the Euro Zone, although May is not ruled out for the Fed (with a 70% probability)4 nor April for the ECB (50% probability).4 Investors have eliminated the possibility of easing deriving from the March meetings.

3. Markets

In the bond market, the adjustment of expectations has resulted in a rebound in US and Euro Zone government bond yields.

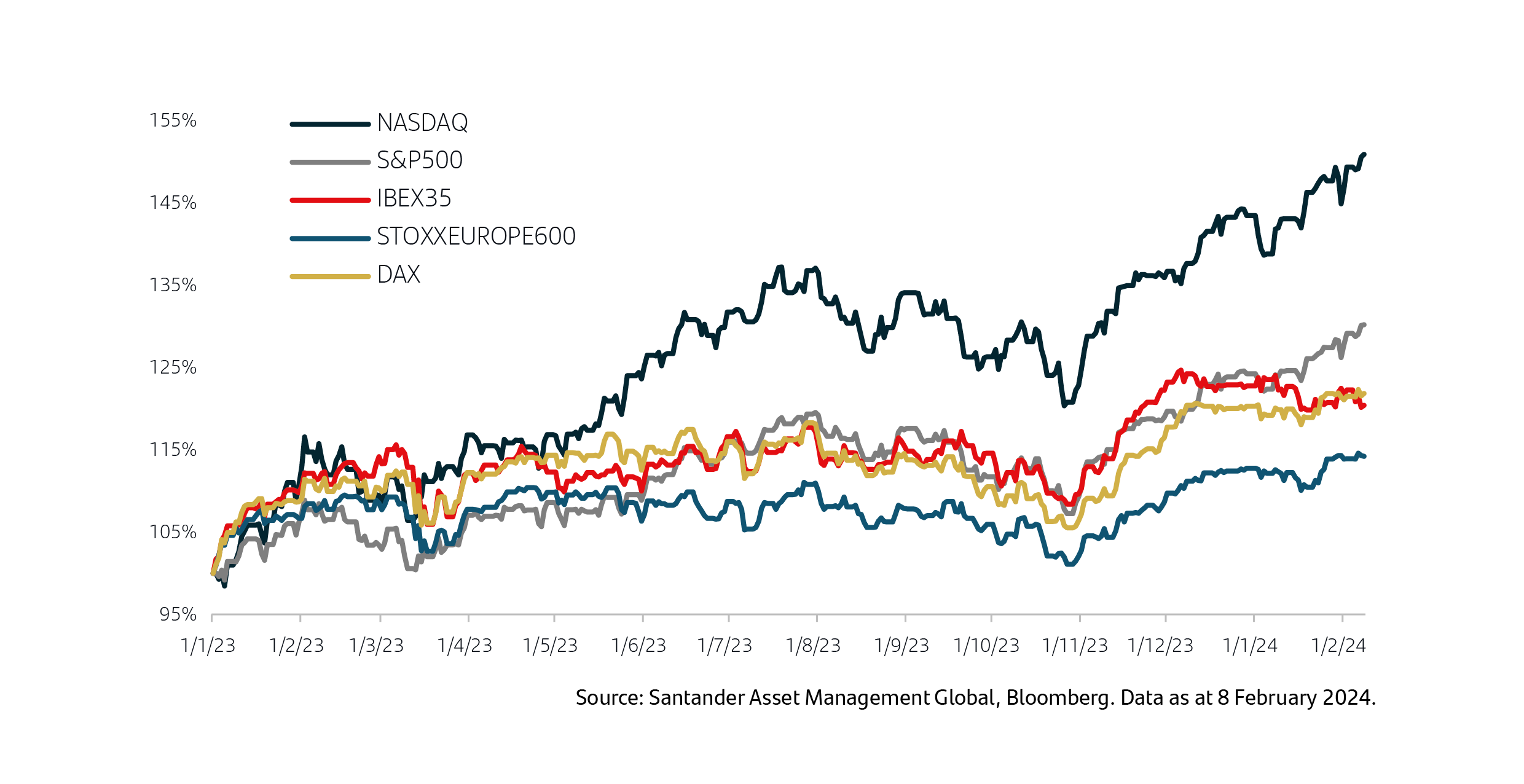

For stock markets, attention is still focused on 2023’s fourth quarter earnings season. The US reporting is more advanced, where more than 60% of S&P 500 companies have already released their results.4 Of these, 81% have exceeded estimates, also exceeding the historical average of 76%.4 In sales, the ratio of positive surprises is 63%, in line with the historical average.4 So we can feel confident to qualify this earnings season as favourable, which reflects the gain of nearly 6% (to 9 Feb 2024) in the S&P 500 Index so far this year.5

In Europe, around 40% of the Euro STOXX 600 have released their earnings and positive surprises sit below 50%.4 Although more data would be preferable to paint a clearer picture, the results are weaker than in the US and reflect the higher pace of growth in the US, as well as the difference in sectoral composition between the two markets. In any case, the favourable factors in the background support the European stock exchange that posted year-to-date gains in the Euro STOXX 600 +1.3% and Euro STOXX 50 +4.5% (to 9 Feb 2024).4

Stock markets since 2023

Market update

Most of the major indexes moved higher over the week, with the S&P 500 Index reaching new highs and breaching the 5,000 threshold for the first time.6 Meanwhile, the Euro STOXX 600 Index made some progress on the back of some reasonably strong company earnings updates, but the likelihood of interest rates staying higher for longer curbed the extent of gains. Italy led the pack in terms of progress, followed by France, with Germany little changed but remaining near its record high. In contrast, the UK’s FTSE 100 Index fell slightly.7

Japan’s stock markets posted gains, with the Nikkei 225 reaching a 34-year high on yen weakness.7 2024 has seen increased foreign investor interest in Japanese shares on the back of a solid earnings season and Bank of Japan (BoJ) monetary support. Finally, Chinese markets rallied in a holiday-shortened week as the government’s latest raft of stimulus measures offset concerns about deepening deflation.7

The value of seeking guidance and advice

It is important to seek advice and guidance from a professional financial adviser who can help to explain how to build an appropriate financial plan to match your time horizons, financial ambitions and risk comfort. If you already have a plan in place or have already invested, it is important to allocate time to review this to ensure this remains on track and appropriate for your needs.

Investing can feel complex and overwhelming, but our educational insights can help you cut through the noise. Learn more about the Principles of Investing here.

Note: Data as at 15 February 2024. 1Reuters, 25 January 2024, 2U.S. Bureau of Labor Statistics, 2 February 2024, 3U.S. Bureau of Labor Statistics, 31 January 2024, 4Santander Asset Management Global & Bloomberg, 8 February 2024, 5FE Analytics, 9 February 2024, 6Reuters, 9 February 2024, 7Reuters, 13 February 2024

Important information

For retail distribution.

This document has been approved and issued by Santander Asset Management UK Limited (SAM UK). This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities or other financial instruments, or to provide investment advice or services. Opinions expressed within this document, if any, are current opinions as of the date stated and do not constitute investment or any other advice; the views are subject to change and do not necessarily reflect the views of Santander Asset Management as a whole or any part thereof. While we try and take every care over the information in this document, we cannot accept any responsibility for mistakes and missing information that may be presented.

The value of investments and any income is not guaranteed and can go down as well as up and may be affected by exchange rate fluctuations. This means that an investor may not get back the amount invested. Past performance is not a guide to future performance.

All information is sourced, issued, and approved by Santander Asset Management UK Limited (Company Registration No. SC106669). Registered in Scotland at 287 St Vincent Street, Glasgow G2 5NB, United Kingdom. Authorised and regulated by the FCA. FCA registered number 122491. You can check this on the Financial Services Register by visiting the FCA’s website www.fca.org.uk/register.

Santander and the flame logo are registered trademarks.www.santanderassetmanagement.co.uk