The return of sustained higher inflation has triggered sharp increases in interest rates to cool demand. However, policymakers are faced with a combination of challenges that arguably will not be solved by just increasing the cost of borrowing. Rising prices have forced many employers to increase wages at their highest rate for more than a generation. Pensioners have also benefited from sharp rises in earnings due to the ‘Triple Lock’ introduced in 2010. Why is the current policy making matters worse for the Bank of England, and how might this affect future interest rate policy? Simon Durling, from Santander Asset Management, shares his thoughts in this week’s State of Play.

Key highlights from this week’s State of Play

- Triple lock

- Unemployment and wages update

- Market update

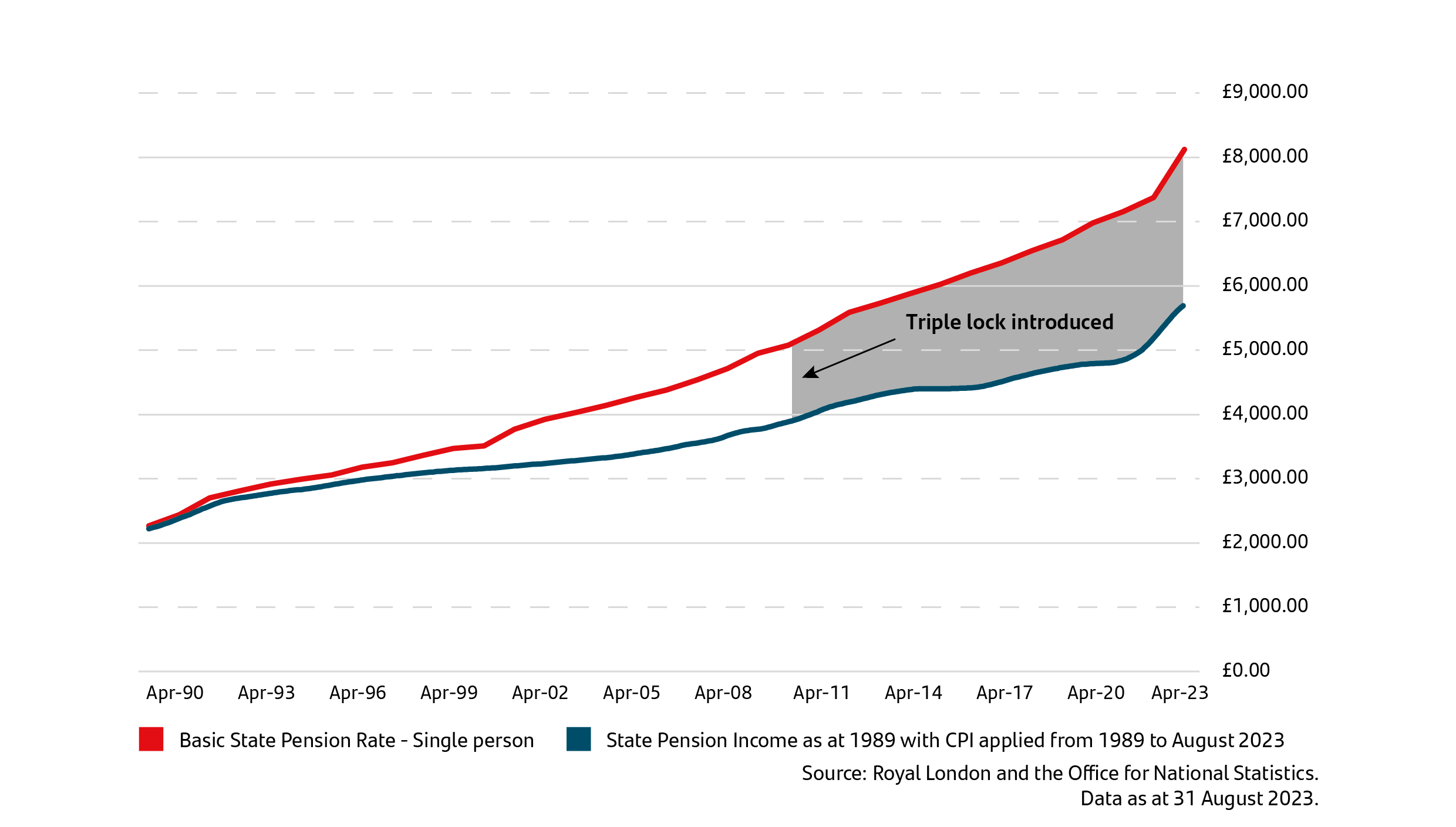

Triple lock introduction

The aftermath of the general election in May 2010 created an initial political vacuum as no party had secured enough votes to command a majority, forcing leaders to explore a coalition government. The incumbent Labour government led by Gordon Brown was unable to find a compromise with the Liberal Democrat party, leaving Westminster at an impasse. Surprisingly, subsequent meetings took place between the leader of the Conservative Party, David Cameron, and Nick Clegg, leader of the Liberal Democrats, who agreed to work together in the national interest, forming a coalition government.1 This coalition introduced several policies that remain to this day, including increasing the basic minimum wage and the personal tax allowance to help the lowest-paid. However, arguably the most financially impactful policy introduced was the ‘Triple Lock’ for the State Pensions.

In an interview with Andrew Marr for the BBC in 2014, the Prime Minister, David Cameron, explained the principle of the original introduction: "I want people when they reach retirement to know that they can have dignity and security in their old age. People who have worked hard, who have done the right thing, who have provided for their families, they should then know they will get a decent state pension and they don't have to worry about it lagging behind prices or earnings and I think that's the right choice for the country."2

The ‘Triple lock’ was first introduced to the UK State Pension in 2010 as a guarantee that it would not lose value and rise at least in line with inflation. The three-way guarantee means that each year, the state pension increases by the highest of the following three measures:

- Average earnings

- Inflation as measured by the Consumer Price Index (CPI)

- 2.5%

In other words, if average earnings were to increase by 5%, the State Pension would also rise by 5%. But if neither average earnings or inflation rises by over 2.5%, the State Pension will still grow by this minimum amount.3 Ever since 2010, pensioners have benefited from a generous increase in their state pension income when compared to the previous 30 years.4

Chart shows the significant increase to the State Pension after the Triple Lock Policy was introduced, especially when compared to inflation over that time period

Based on the latest earnings data announced by the Office for National Statistics earlier this week and assuming inflation numbers do not exceed earnings, the Basic State Pension is due to rise by 8.5% in April, a weekly increase of £13.30.5 The annual increase of £691.60 takes the total for the year to £8,814, and for those receiving the new flat-rate State Pension, who reached State Pension Age after April 2016, the rise is set to be £17.35 a week, or £902.20 a year - taking the total for the year to £11,502.5 The increase due in April will be the second significant increase in the State Pension in two years, after a 10.1% increase in April of this year.6

Triple lock ripple effects

Many of you may wonder why the Triple Lock has any bearing on investment markets or future financial policy.The reason is that policymakers have been battling to bring down the rise in prices to their long-term target of 2%. If wages increase by too much, this makes the challenge much harder. High wages feed into higher consumption as people tend to spend some of the additional earnings they receive. In addition, this can have an impact that is known as the second-round effect. This is caused by employers who pay their workers higher wages and try to pass much of these wage rises onto the prices they charge for their goods and services, increasing price rises further. Obviously, pensioners are paid by the government, so they do not form part of the second-round effects but still contribute to economic consumption as their pension incomes increase at the same time they receive higher interest on their savings, assuming they have sufficient savings to benefit from higher rates. The other important factor is the cost of maintaining the Triple Lock policy in the long term. Politicians on all sides recognise how sensitive the subject is and with less than 18 months before a general election is due to be held, the major parties are keeping their cards close to their chests about whether they plan to change the methodology of how it is calculated in the future. It remains to be seen how this unfolds, but for now, many retired people will welcome the significant boost in their pension earnings.

Employment and wages update

According to the Office for National Statistics UK (ONS), wages grew at the fastest pace on record in the three months to July, despite the jobs market continuing to weaken as unemployment rose alongside a slowing of job hires.5 The annual growth in average pay, excluding bonuses, remained at 7.8%, the same as last month and the highest rate since 2001, when comparable records began.5 Total pay grew 8.5%, elevated by one-off payments to NHS workers and civil servants following pay settlements designed to end recent strike action.5 Average wages are now growing faster than rising prices, which will provide some light relief for many households.

On unemployment, the ONS reports state: ‘The unemployment rate for May to July 2023 increased by 0.5% on the quarter to 4.3%. The increase in unemployment was largely driven by people unemployed for up to 12 months. The economic inactivity rate increased by 0.1 percentage points on the quarter, to 21.1% in May to July 2023. The increase in economic inactivity during the latest quarter was driven by people aged 16 to 24 years. Those inactive because of long-term sickness increased to another record high.’5

The wage rises will be an ongoing concern for the Bank of England Monetary Policy Committee, which is due to meet next week to decide on interest rates. Second-round effects, as described earlier, risk inflation being embedded as workers are encouraged to negotiate with their employers for higher wages, which in turn is passed onto the end prices charged for their goods and services, keeping inflation higher for longer. The only sliver of good news in the statistics was the 14th consecutive fall in jobs vacancies to below one million. Vacancies fell by 64,000 to 989,00, although still much higher than the previous running average before the pandemic began.5

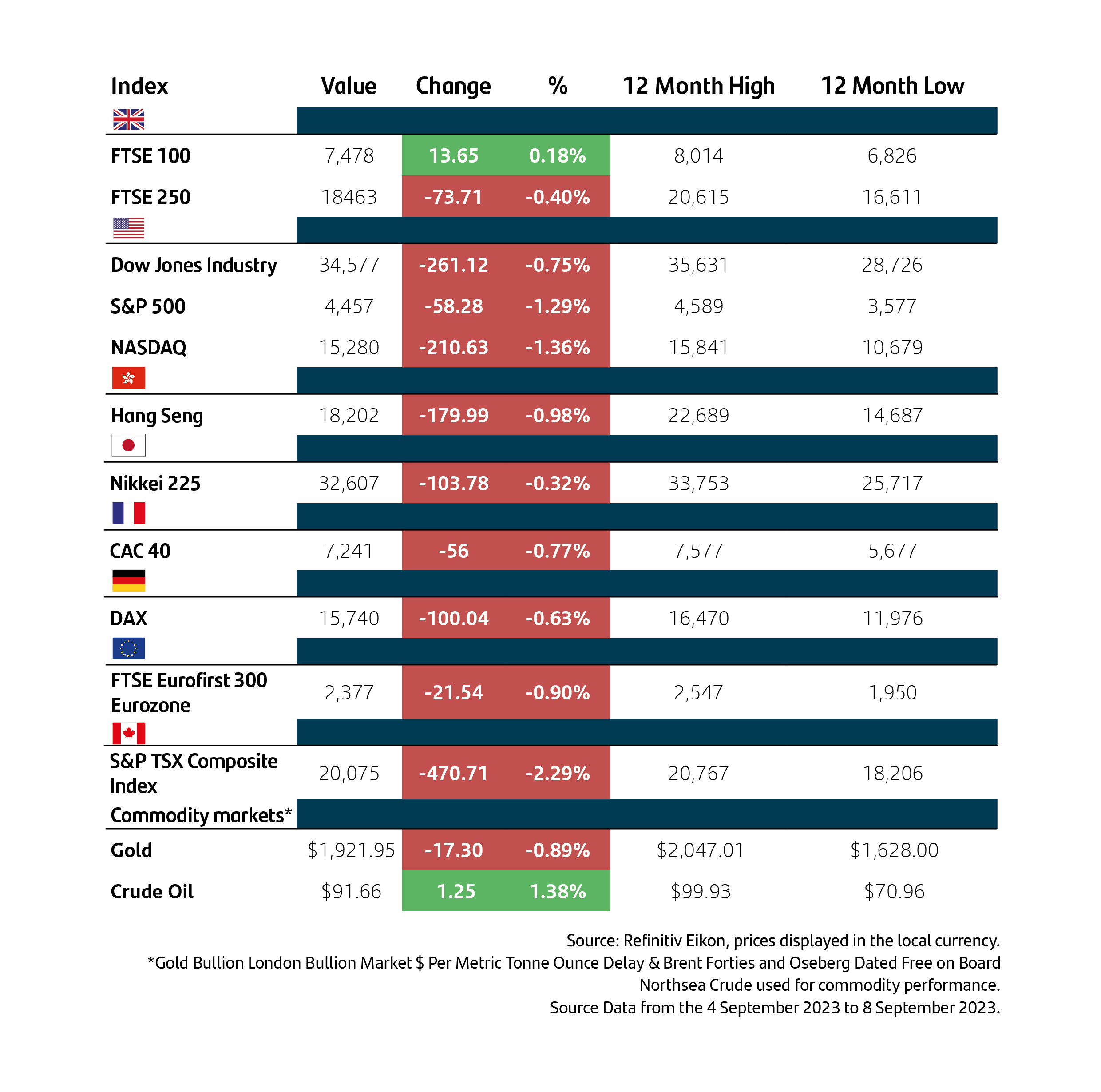

Market update

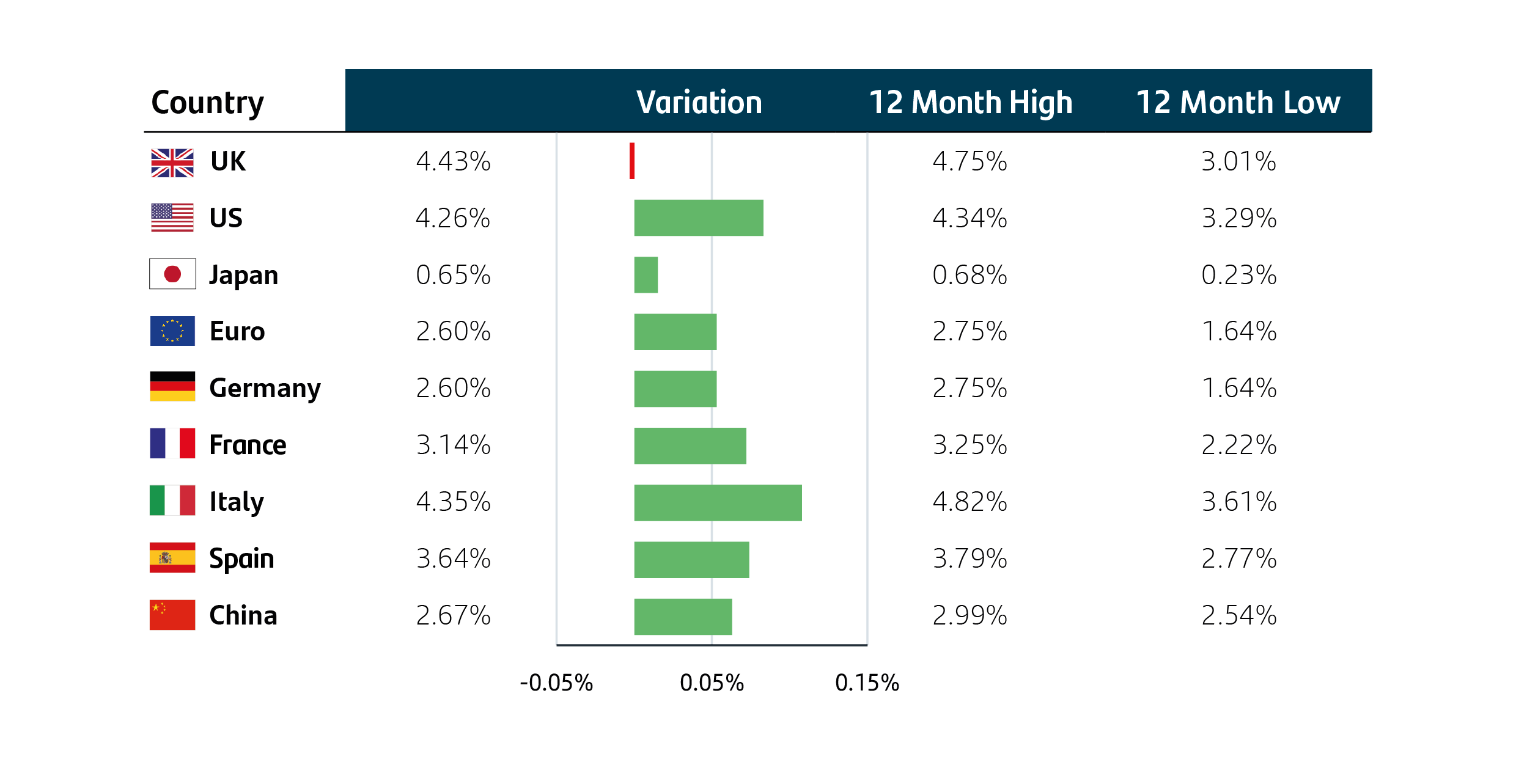

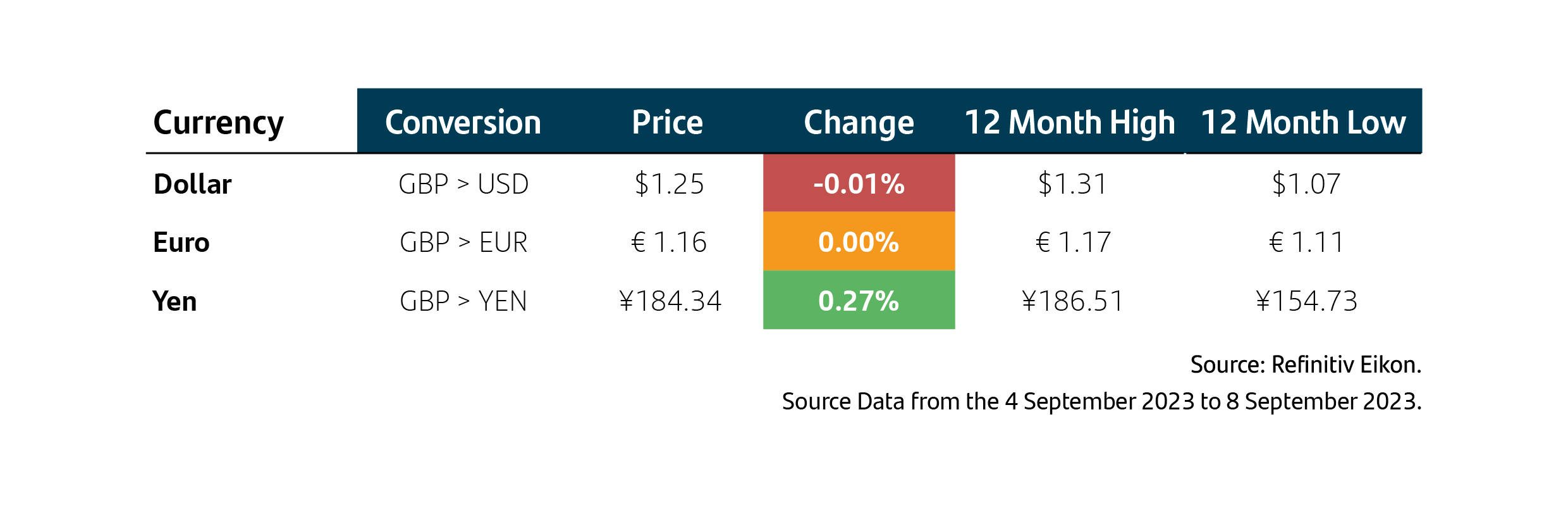

Investment markets were broadly flat in the last trading week as market participants await important economic data releases over the this week and next. The US, Europe and the UK are set to release jobs and inflation data alongside all three central banks due to make crucial decisions about interest rates. Most investment market participants are expecting the Federal Reserve to pause on raising rates next week, but are more divided about whether either the Bank of England or the European Central Bank will increase rates by 0.25%.7 The US market fell slightly as Apple’s value dropped $200bn last week as concerns about Beijing-led interventions over recent months dented investor confidence.8 Chinese government employees have recently been told to stop using Apple products at work.9 China represents a large portion of Apple’s overseas market as well as being a major manufacturing hub for making and distributing their products, especially their iPhones. Bond yields barely moved over the week as bond market investors wait nervously for all of the economic data to be factored in and the subsequent response from central banks.

The value of seeking guidance and advice

It is important to seek advice and guidance from a professional financial adviser who can help to explain how to build an appropriate financial plan to match your time horizons, financial ambitions, and risk comfort. If you already have a plan in place, or have already invested, it is important to allocate time to review this to ensure this remains on track and appropriate for your needs.

Performance 10-year bond yields

10-year bond yields Currencies

Currencies

Investing can feel complex and overwhelming, but our educational insights can help you cut through the noise. Learn more about the Principles of Investing here.

Note: Data as at 14 September 2023. 1The Guardian, 12 May 2010. 2BBC, 5 January 2014. 3Commons Library Parliament, 4 February 2021. 4Royal London, 30 April 2023. 5Office for National Statistics, 12 September 2023. 6BBC, 12 September 2023. 7Refinitiv Eikon, 13 September 2023 . 8Financial Times, 12 September 2023. 9Wall Street Journal, 6 September 2023.

Important information

For retail distribution.

This document has been approved and issued by Santander Asset Management UK Limited (SAM UK). This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities or other financial instruments, or to provide investment advice or services. Opinions expressed within this document, if any, are current opinions as of the date stated and do not constitute investment or any other advice; the views are subject to change and do not necessarily reflect the views of Santander Asset Management as a whole or any part thereof. While we try and take every care over the information in this document, we cannot accept any responsibility for mistakes and missing information that may be presented.

The value of investments and any income is not guaranteed and can go down as well as up and may be affected by exchange rate fluctuations. This means that an investor may not get back the amount invested. Past performance is not a guide to future performance.

All information is sourced, issued, and approved by Santander Asset Management UK Limited (Company Registration No. SC106669). Registered in Scotland at 287 St Vincent Street, Glasgow G2 5NB, United Kingdom. Authorised and regulated by the FCA. FCA registered number 122491. You can check this on the Financial Services Register by visiting the FCA’s website www.fca.org.uk/register.

Santander and the flame logo are registered trademarks.www.santanderassetmanagement.co.uk