Last week represented a tense week for both investors and borrowers. Crucial decisions about interest rates and, probably more importantly, future expectations were articulated by both the Federal Reserve and the Bank of England. With inflation falling more than expected and the economy in the UK slowing, the battle between the ‘hawks’ and the ’doves’ was a close call. What can investors and borrowers expect in the months ahead? Simon Durling, from Santander Asset Management, shares his thoughts in this week’s State of Play.

Key highlights from this week’s State of Play

- Hawk or dove?

- Slow cooked or chargrilled?

- Market update

Hawk or dove?

Following last week’s close call on the decision to pause rises in UK interest rates after 14 consecutive meetings in which the Bank of England Monetary Policy Committee (MPC) raised rates, it is worth pausing to remind ourselves of their role and what each member may prefer in their approach to managing price stability and future economic growth. So, why are they described as either a ‘hawk or a ‘dove’? Firstly, it is important to remember the primary purpose of central banks, which is to maintain stable prices and full employment to enable stable economic growth. They are responsible for setting interest rates, controlling how much money is in the economy, and guiding an economy to maintain rising prices around a long-term target of 2%.1

When a policymaker is described as a dove, it is because of their belief that lower interest rates and an increase in the money supply lead to higher economic growth and more jobs, even if this means inflation remains at times above the ideal target. Hawks prefer to limit inflation as their primary goal, believing that maintaining lower price rises helps deliver more sustainable economic growth in the long-term. They are prepared to increase interest rates and restrict money supply to achieve this. While most policymakers tend to be either-or, there are some who follow a middle path and are referred to as centrists.2 Importantly, central banks will normally ensure the experts tasked with making such important decisions on monetary policy are a mixed group, so a strong debate can underpin the decisions they make each time they meet. Also, depending on where in the economic cycle the economy reaches, hawks can become more dovish and vice versa.

If you follow both the meeting outcomes, the published minutes from each meeting, and the subsequent interviews conducted by different members of the MPC, you will notice they do not always agree on whether to increase interest rates or by how much. This is important because each member assesses the same economic data but often arrives at slightly different conclusions. This is a reflection on their expert opinion on the best way to manage monetary policy to achieve the committee’s objectives on inflation, employment, and economic growth. Their views are typically described as either more dovish or more hawkish as a result. A healthy mix of both is considered a more consistent approach to decision making.

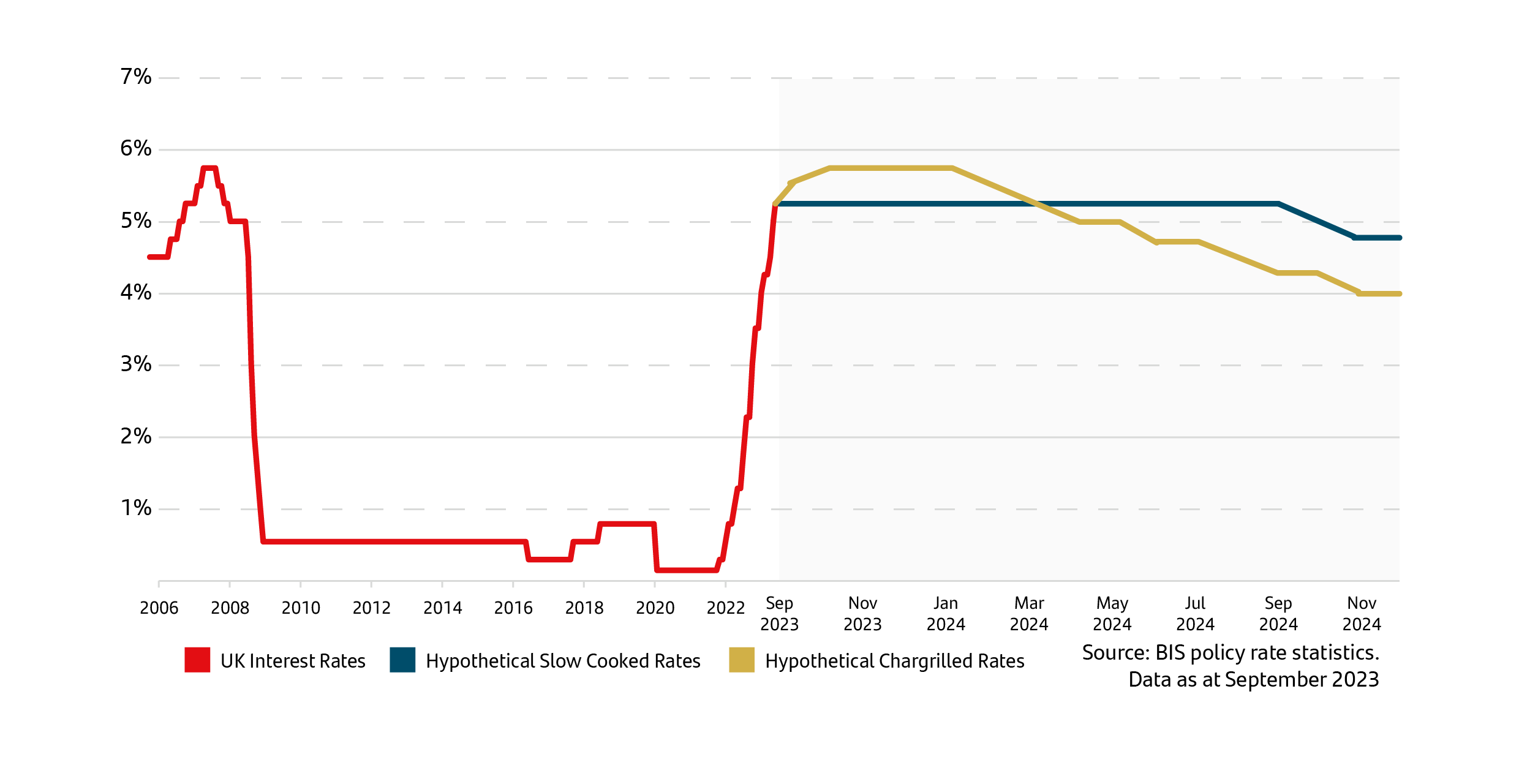

Slow cooked or chargrilled?

The nine members of the Monetary Policy Committee you see in the image above all have slightly different thoughts on how monetary policy should be implemented to achieve the bank’s objectives of stable prices and economic growth through the control of both interest rates and money supply (how much money is in the wider economy). Unusually (compared to other central banks), the MPC reports back after their meeting not only the decision on interest rates, but also which members voted and for what course of action, whether this is to raise, cut or hold rates the same.

The vote this time round was 5 votes for hold versus 4 votes to hike rates. Andrew Bailey, the governor, thought inflation was falling fast enough to warrant the first pause in rates since November 2021. Chief economist Huw Pill, deputy governors Dave Ramsden and Ben Broadbent, and an external member, Swati Dhingra, also voted to keep rates the same. The four ‘hawks’ who preferred to raise rates to 5.5% were Sir Jon Cunliffe and the external members Megan Greene, Jonathan Haskel, and Catherine Mann. So, why do these policymakers disagree, and is that intended? Firstly, the strategy for bringing down inflation is the collective goal of the committee, regardless of their views on how to do it. To make this easier to understand, I will use an analogy: Slow cooked or chargrilled’?

Interest rate possible path

As I am sure you will all be aware, whether you are cooking meat, fish, vegetables, or any other type of food you choose, a recipe and the way this is cooked can vary even for the most basic of meals. For me, deciding on interest rates in the current market environment makes me think of the cooking analogy. During the summer, many of us like to cook barbeques over hot coals. If you are like me, I am always deeply worried I will burn the outside of the meat but not cook the meat properly on the inside. Using this method, meat can cook very quickly to achieve the desired taste. Others prefer to cook a dish on a much slower heat, recognising that it will take much longer to achieve a tasty dish. Lamb, is a perfect example of a meat that can be delicious when slow cooked. So how does this have anything to do with interest rates?

The MPC at the Bank of England decided to pause rates last week. However, they did expect rates to stay higher for longer. Some of the members would prefer to raise rates and then cut them – a bit more chargrilled – hot for a short period, and then ease rates after the medicine has worked. Because the slim majority decided to pause, they may have to keep rates at these levels for longer before they decide to cut rates – slow cooked, rather than chargrilled. The ‘hawks’ would prefer to raise rates further to squeeze demand until inflation is closer to the long-term target of 2%. They would prefer to go too far with rate rises than not far enough, as they are concerned that inflation could become embedded at an ongoing level well above 2%. Once the battle with rising prices was clearly won, they would then be prepared to cut rates to stimulate the economy.

Importantly, at the start of August, the Chancellor, Jeremy Hunt, announced that Sir Jon Cunliffe, the Deputy Governor, who has been in post for more than a decade, will be leaving and replaced with another long servant of the bank, Sarah Breeden.3 Her first day is 1 November, the day before the important MPC meeting. Immediately after the last meeting, many commentators that I observed in the press expect her to vote in line with the Governor, Andrew Bailey, on the grounds that it would be early to disagree with her new boss just 48 hours into taking up her new post, moving the voting balance 6-3 in favour of keeping rates on hold. Obviously, at this stage, it is unclear whether Breeden will lean towards favouring looser or tighter monetary policy, given that her previous role managing financial stability strategy did not require her to vote on interest rate decisions. We will wait and see what she decides.

Market update

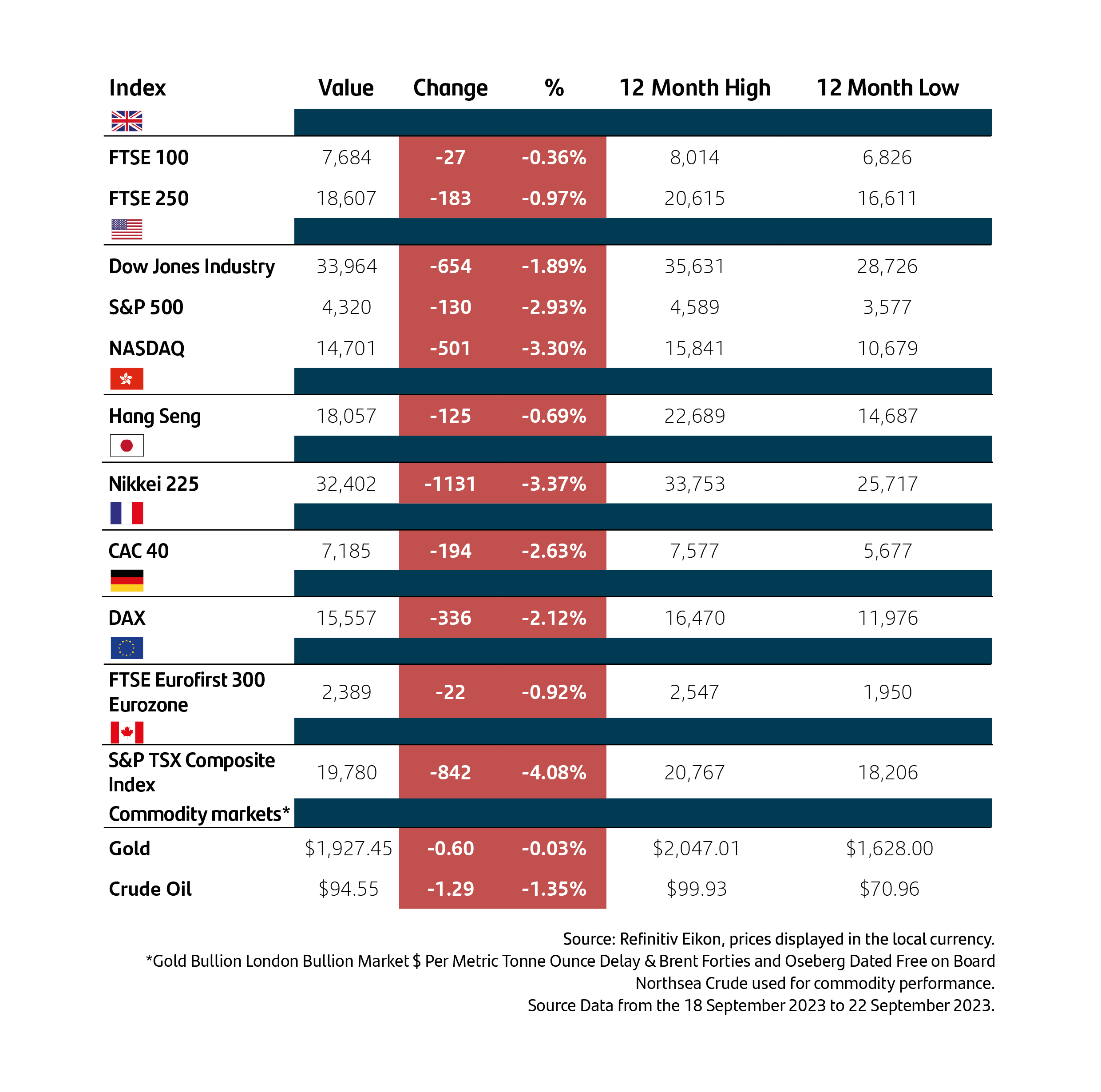

Last week stock markets continued their falls after Jerome Powell, the Chair of the Federal Reserve, warned investors on Wednesday that they may still increase interest rates in November and change their expectations for rate cuts next year. In his press conference following their decision to pause rates, he explained they only expected to cut rates twice in 2024, rather than the four cuts positioned previously. Higher rates for longer saw US bond yields rise and share prices fall, especially in the technology sector, as the NASDAQ fell more than the broader market.4

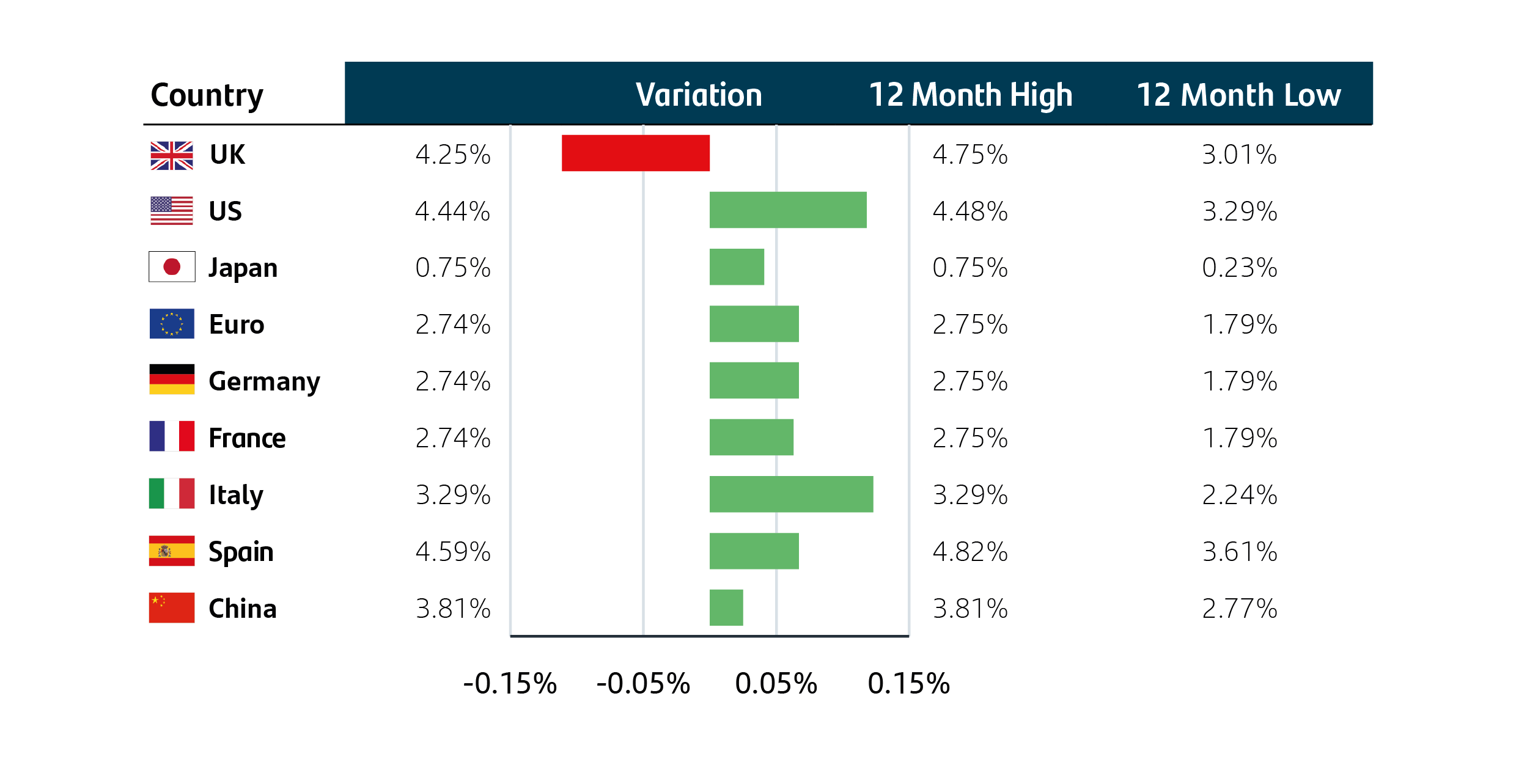

Despite the MPC surprising markets with their decision to pause rate rises, the initial sharp fall in both the pound and UK bond yields on Tuesday, directly after the inflation numbers were better than predicted, didn’t lastvery long. UK 10-year Government Bond yields have fallen from their recent peak of 4.75%, and as of the time of writing, they were 4.2%.4 For savers and borrowers, the rate available to them is very much dependent on what is known as the ‘UK 5-year Swap rate’. This has fallen significantly from the most recent peak of 5.67% to a much lower rate of 4.7%.4 This is reflected in the savings rates over one year being higher than over two, three or even five years.5 Typically, you would be rewarded for tying up your money for longer with better interest. This change reflects market expectations that the current competitive rates may be either at their peak or very close to it and that rates will start to fall at some point next year.

The value of seeking guidance and advice

It is important to seek advice and guidance from a professional financial adviser who can help to explain how to build an appropriate financial plan to match your time horizons, financial ambitions, and risk comfort. If you already have a plan in place, or have already invested, it is important to allocate time to review this to ensure this remains on track and appropriate for your needs.

Performance

10-years bond yields

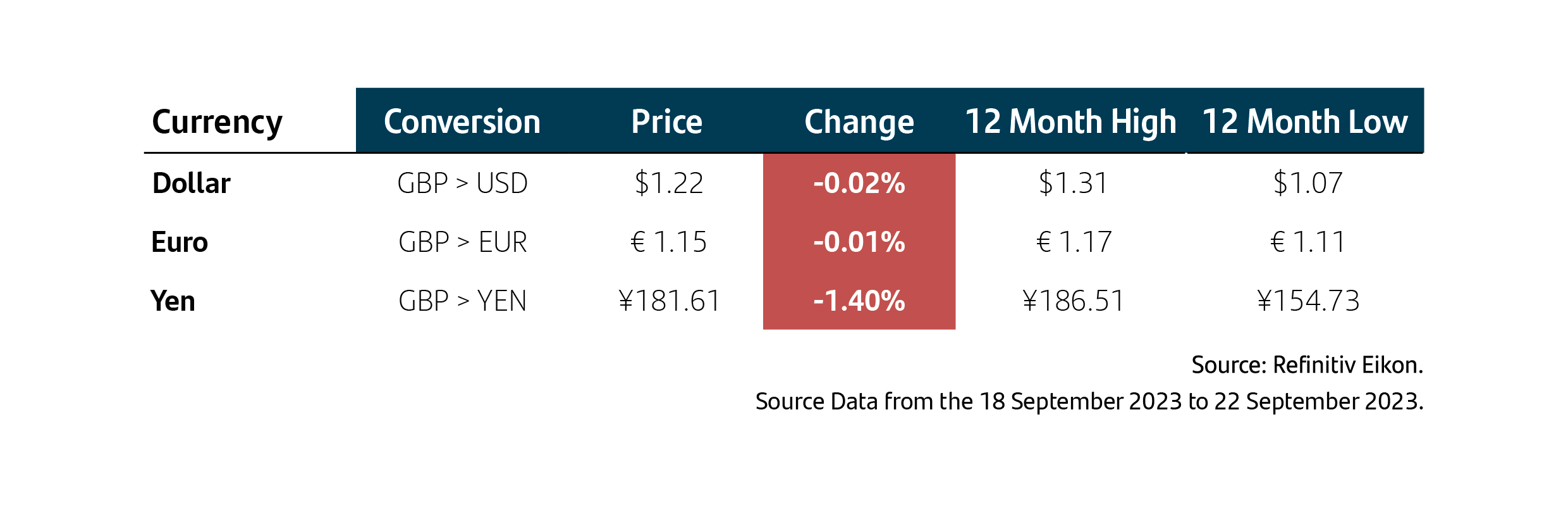

Currencies

Investing can feel complex and overwhelming, but our educational insights can help you cut through the noise. Learn more about the Principles of Investing here.

Note: Data as at 28 September 2023. 1Bank of England, 1 August 2023. 2London School of Economics, 21 November 2007. 3CityAM, 1 August 2023. 4Investing.com, 25 September 2023. 5Money Saving Expert, 25 September 2023.

Important information

For retail distribution.

This document has been approved and issued by Santander Asset Management UK Limited (SAM UK). This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities or other financial instruments, or to provide investment advice or services. Opinions expressed within this document, if any, are current opinions as of the date stated and do not constitute investment or any other advice; the views are subject to change and do not necessarily reflect the views of Santander Asset Management as a whole or any part thereof. While we try and take every care over the information in this document, we cannot accept any responsibility for mistakes and missing information that may be presented.

The value of investments and any income is not guaranteed and can go down as well as up and may be affected by exchange rate fluctuations. This means that an investor may not get back the amount invested. Past performance is not a guide to future performance.

All information is sourced, issued, and approved by Santander Asset Management UK Limited (Company Registration No. SC106669). Registered in Scotland at 287 St Vincent Street, Glasgow G2 5NB, United Kingdom. Authorised and regulated by the FCA. FCA registered number 122491. You can check this on the Financial Services Register by visiting the FCA’s website www.fca.org.uk/register.

Santander and the flame logo are registered trademarks.www.santanderassetmanagement.co.uk