All central banks chose to pause interest rate rises last week. How will markets react upon reflection and what can investors expect? Those who look for opportunities and positive outcomes are often described as ‘bulls’ and others who expect the worst are called ‘bears’. Where do these terms originate from and what do they mean? Given that current economic data and company earnings are mixed, pointing to uncertainty, who will win the battle in the months ahead? Simon Durling, from Santander Asset Management, shares his thoughts in this week’s State of Play.

Key highlights from this week’s State of Play

- Battle of bulls and bears

- Spreading your bets

- Market update

The battle between bulls and bears

In recent weeks, you could be forgiven for questioning why investment markets appear to be riding high one week only for them to sharply fall in value the next. This change in mood or sentiment may be confusing for the average retail investor who finds investments and the financial world bewildering. Last week, both the US and UK central banks decided to pause interest rate rises but with a cautioning notice about the possible need to act once more if rising prices break their downward trend. This ends a prolonged period of rising interest rates and what is known as financial tightening (reducing the amount of money available in the financial system). So, what happens next? Depending on investor views and opinions, they may see the peak in interest rates as an investment opportunity. However, they may be of the opinion that the rate rises have yet to inflict the total cost on both individuals or the wider economy and are pessimistic about the months ahead. This difference in mindset is often referred to as either ‘bullish or bearish’. Where do these terms originate and what do they mean?

Bear skins

The most common way of explaining the difference between a ‘bear’ investor or a ‘bull’ investor is in reference to how they attack. A bull thrusts its horns upward, symbolizing rising prices, while a bear swipes its paws downward, representing falling prices.1 However, the term bear, depending on which historian you choose to believe, can be dated back before the use of the word bull to describe the opposite, and long before investment markets were fully created. Etymologists (a person who studies the origin and history of words) believe the term 'bear' comes from trade, as it relates to the selling of bear skins.2 From a technical perspective a ‘bear’ market is one which has fallen in value by 20% or more from the most recent peak.3 There is a difference between being a ‘bear’ investor, who tend to take advantage of poor economic conditions, and becoming ‘bearish’ - meaning you have become more pessimistic or worried about the future.

The explanation provided

Etymologists point to a proverb warning that it is not wise "to sell the bear's skin before one has caught the bear." It refers to traders (otherwise known as ‘bearskin jobbers’) who would sell bear skins before they were caught, hoping to secure a higher price by trading in advance on the expectation there would be plenty of supply, leading to the fall in price. By the eighteenth century, the term bearskin was being used in the phrase "to sell (or buy) the bearskin" and in the name "bearskin jobber," referring to one selling the "bearskin." Bearskin was quickly shortened to bear, which was applied to stock that was being sold by a speculator, with the speculator selling stock.2

Bulls win more than bears

A bull market is deemed a rising market where investors are optimistic and buying more investments, driving values higher.3 Again, like a bear market, a bull market tends to be measured when it reaches 20% higher than a recent low. If you apply common sense to this balance between the bull and bear, given stock markets have risen exponentially over history, clearly bull investors have won more times than bear investors. It doesn’t mean that recognising a bear market and the characteristics of investors when financial conditions become gloomier is not important. Overtime, retail investors who invest at the appropriate risk, for the right length of time and remain patient tend to be rewarded more than those who panic. Importantly, your own individual circumstances may differ and remaining invested may not be the best decision, so it is always important to seek guidance from a professional financial adviser before making a decision that you may come to regret.

Spreading your bets

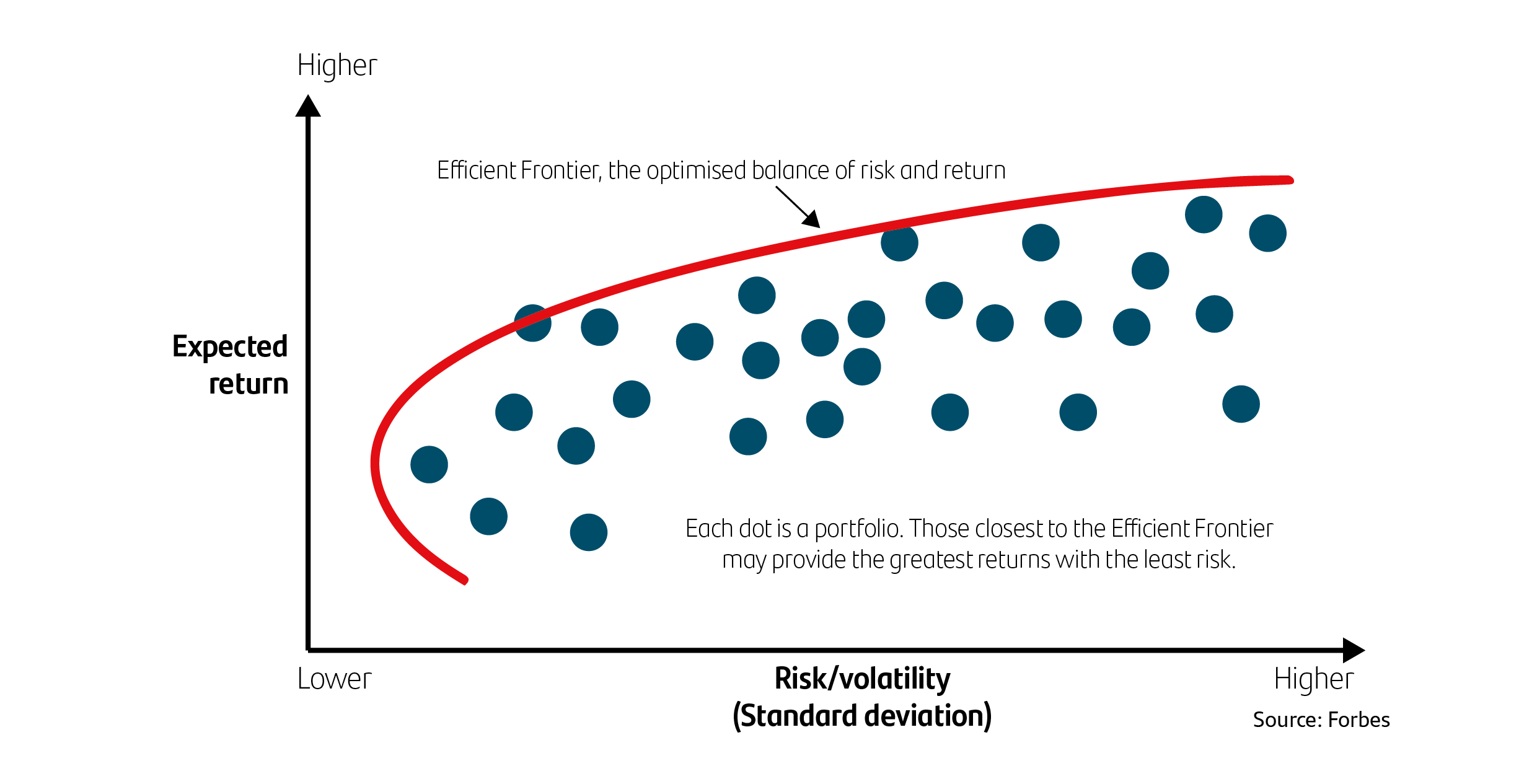

American economist Harry Markowitz pioneered a theory that was published in 1952 titled ‘Portfolio Selection’, arguing that assets should not be viewed in isolation, but within an overall portfolio. Modern Portfolio Theory is a method for selecting different investments within a portfolio to maximise returns for an agreed level of risk.4 Many aspects of this theory are still integral to how investment solutions are designed and managed by investment companies. Often, these solutions will be recommended by a professional adviser, who will first evaluate a client’s attitude towards investment risk, assess their circumstances alongside their long-term goals, and then recommend the appropriate investment solution that best matches all these factors and aims to achieve their objectives. If you look back over history, different asset classes like shares, bonds and property at times behave very differently and this is measured using correlation.4 If assets are negatively correlated, when one asset class rises in value, the other will fall, and vice versa. If they are positively correlated, then they will rise and fall at the same time. The degree to which they change in price in relation to one another is also measured. Clearly, this correlation or relationship between asset classes is not constant and is always changing. However, these differences allow for an assessment of what proportion of different assets should be included in the original asset allocation depending on the objectives, strategy, time horizon and risk profile of the investment solution matched to the investment needs and risk appetite of an investor, with the intent to deliver a smoother investment journey. This principle is called diversification.

Modern portfolio theory Efficient Frontier

In practice, diversification sees investment managers using different asset classes in varying proportions at different stages throughout an investment journey, changing the shape and allocations depending on market conditions and the short-term outlook. When an investment solution is recommended, it should align with the investor’s objectives, time frame and attitude to risk. Once the client invests in the recommended solution, the investment manager’s task is to manage the solution in line with the fund’s long-term investment objectives and risk profile. The rules and boundaries set to help stay within this agreed risk level restrict how much investment managers can make changes to investment portfolios. So, in rare circumstances, asset classes are very positively correlated for a sustained period. When shares and bonds are all falling in value at the same time, the options available to avoid or mitigate these falls can be very limited. This can mean most investors, regardless of how comfortable they are with risk, can experience falling investment values at the same time.

My explanation to try and simplify this concept is to think of your investment as a long-haul flight to a faraway destination with your fund manager as your pilot and the other passengers as fellow investors in the same fund or portfolio. Ideally, the pilot would look ahead at the impending weather, the direction and strength of the winds at different altitudes and navigate the most efficient route to help achieve the smoothest and most comfortable journey for the passengers (the investors) reaching their desired destination. Depending on how unpredictable the weather systems are or whether there are large the storms are along the way, regardless of what changes in coordinates the pilot chooses to make, they may not be able to avoid all of the turbulence, especially when the conditions are so changeable on the journey. In reality, especially for passengers who dislike flying, this can feel very scary. Given what has happened in the last few years and how different asset classes have fallen in value at the same time, many investors are likely to feel very nervous and tending to think the worst. Whilst the first reaction is to expect the pilot to mitigate the turbulence or fly around it, sometimes this just isn’t possible. Remember, investing is a long journey better thought about in decades, not days.

Market update

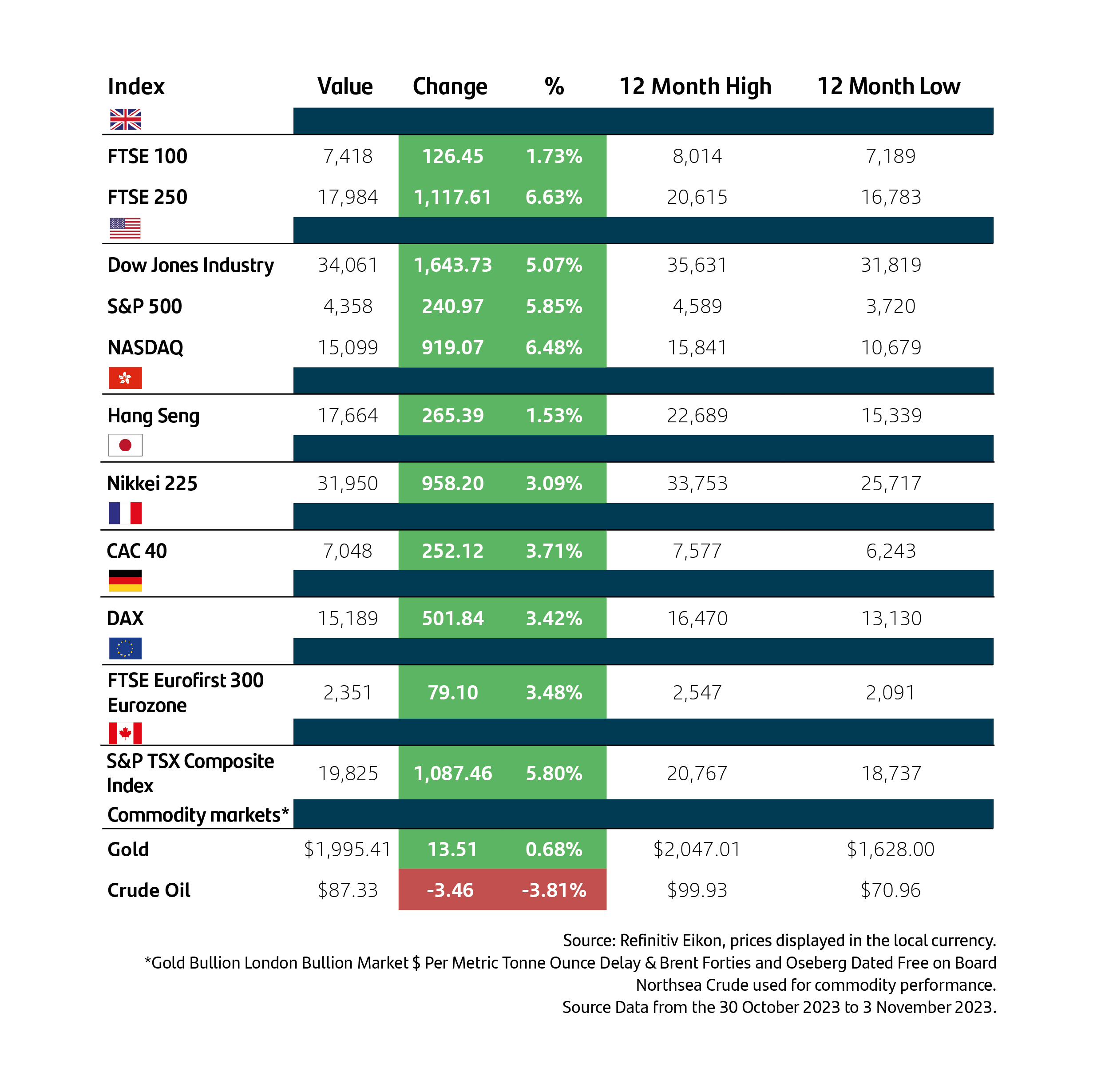

I have often explained that investment markets like certainty. When surprises come along, asset classes like shares and bonds can become much more volatile when investors are unsure of what the immediate future may bring. Last week, we saw for the first time in what seems like a long time that expectations for central banks to not raise interest rates going as forecast.5 Coupled with more economic data pointing to the necessary slowdown, which supports an outlook of price rises continuing to fall, market participants appeared to breathe a sigh of relief. As I have predicted in previous updates, as soon as it appears we are at the peak of rate rises and investors assume that the next move will be a cut, then bond yields should fall (meaning bond values rise) and share prices would also rally. Last week saw the strongest rally in share prices for many months and a significant fall in bond yields as their values recovered. All eyes will now turn to the next round of economic data, which may or may not provide evidence that central banks are winning the war on inflation.

The value of seeking guidance and advice

It is important to seek advice and guidance from a professional financial adviser who can help to explain how to build an appropriate financial plan to match your time horizons, financial ambitions, and risk comfort. If you already have a plan in place, or have already invested, it is important to allocate time to review this to ensure this remains on track and appropriate for your needs.

Performance

10-years bond yields

Currencies

Investing can feel complex and overwhelming, but our educational insights can help you cut through the noise. Learn more about the Principles of Investing here.

Note: Data as at 9 November 2023. 1Investopedia, 8 November 20233. 2Merriam-Webster Dictionary, 7 November 2023. 3Forbes, 24 August 2023. 4Forbes, 26 June 2023. 5World Economic Forum, 3 November. 2023

Important information

For retail distribution.

This document has been approved and issued by Santander Asset Management UK Limited (SAM UK). This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities or other financial instruments, or to provide investment advice or services. Opinions expressed within this document, if any, are current opinions as of the date stated and do not constitute investment or any other advice; the views are subject to change and do not necessarily reflect the views of Santander Asset Management as a whole or any part thereof. While we try and take every care over the information in this document, we cannot accept any responsibility for mistakes and missing information that may be presented.

The value of investments and any income is not guaranteed and can go down as well as up and may be affected by exchange rate fluctuations. This means that an investor may not get back the amount invested. Past performance is not a guide to future performance.

All information is sourced, issued, and approved by Santander Asset Management UK Limited (Company Registration No. SC106669). Registered in Scotland at 287 St Vincent Street, Glasgow G2 5NB, United Kingdom. Authorised and regulated by the FCA. FCA registered number 122491. You can check this on the Financial Services Register by visiting the FCA’s website www.fca.org.uk/register.

Santander and the flame logo are registered trademarks.www.santanderassetmanagement.co.uk