The Bank of England began the journey to normality in December 2021 when they increased interest rates from a mere 0.1% to 0.25%. Today, the Monetary Policy Committee (MPC) at the bank met to decide their next move, with market expectations for the 14th consecutive rise in rates. Did the latest UK inflation data influence the debate about not just this decision but future meetings for the remainder of this year? Importantly, what does this mean for savers and investors? Derek Barrow from Santander Asset Management shares his thoughts in this week’s State of Play.

Key highlights from this week’s State of Play

- Back to normal

- Decision time

- Market update

Back to normal

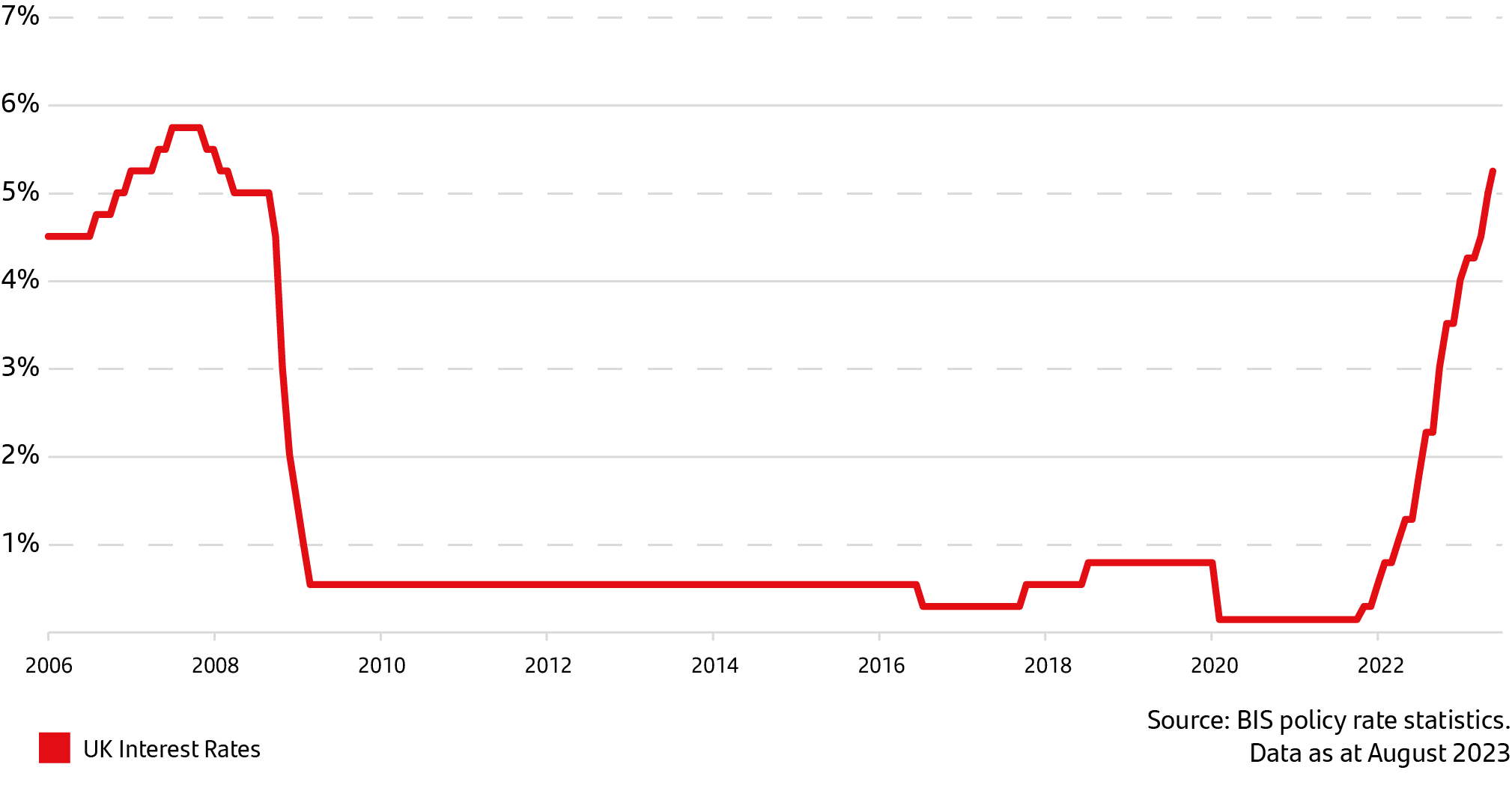

The Bank of England is fast approaching a crucial time when they must decide how high they should raise interest rates to accomplish their task of bringing down inflation to their long-term target of 2%. This month’s meeting will be the 14th consecutive increase in interest rates in the UK, assuming they press ahead with another widely expected raising of the base rate. This journey has been a painful one for both policymakers and the public, as the bank initially had to play catch-up after misjudging the return of rising prices, citing the reasons as temporary and therefore making rate rises unnecessary. Rewind fifteen years to the beginning of 2008, when interest rates stood at 5.5%1, several financial shocks created a dark cloud over the stability of our economic and financial future. Back then, central banks took unprecedented steps to ensure financial stability by slashing rates to near zero and embarking on an untested programme of quantitative easing (QE). In simple terms, this is where central banks create new money, which is used to buy back debt from retail and commercial banks, so they feel that they can lend to businesses and individuals when uncertainty dominates lending decisions.

What at the time was described as a temporary measure lasted 14 years. The pandemic forced economies to press the pause button and restrictions limited economic activity to online consumption, the pent-up demand overwhelmed supply chains once we emerged from global lockdown restrictions. Just before COVID-19 was identified, central banks had finally started to map out a plan to return our financial world back to normal, which I am sure would have been a much slower and gradual increase in interest rates and reduction in the money supply. However, their best laid plans had to be thrown away, as additional easing with more money and lower rates was used to support individuals and businesses during the pandemic. Over a year and a half since the battle to tame inflation began, policymakers face the final stage with an enormous amount of anxiety and concern. A couple of questions many may be asking are: When will they stop raising rates? When will they begin to cut rates in the future?

Decision time

As expected, the Bank of England MPC decided to increase interest rates by 0.25%, citing the bigger fall in inflation last month as a sign that the worst is over on bringing down price rises and, given what lies ahead, a confidence that inflation will continue to fall throughout the remainder of this year.2 While they didn’t commit to pausing rate rises now, there was acknowledgement that depending on economic data in the next few weeks, they may not have to go as high as the market had been pricing in prior to the inflation data release last week. Clearly, hundreds of thousands of mortgage deals are due for renewal over the remainder of this year, with large jumps in borrower’s payments, which act as a brake on consumer spending and help the inflation pressure ease. As State of Play mentioned last week, there are signs that central banks could probably press the pause button now given how long the lag is before higher rates really start to show in the economic numbers. They will argue that it is better to go too far than not far enough. Only time will tell whether their approach will be vindicated in the months ahead. There is certainly no shortage of opinions on what they have done so far or what they should do next.

UK interest rate decisions

Market update

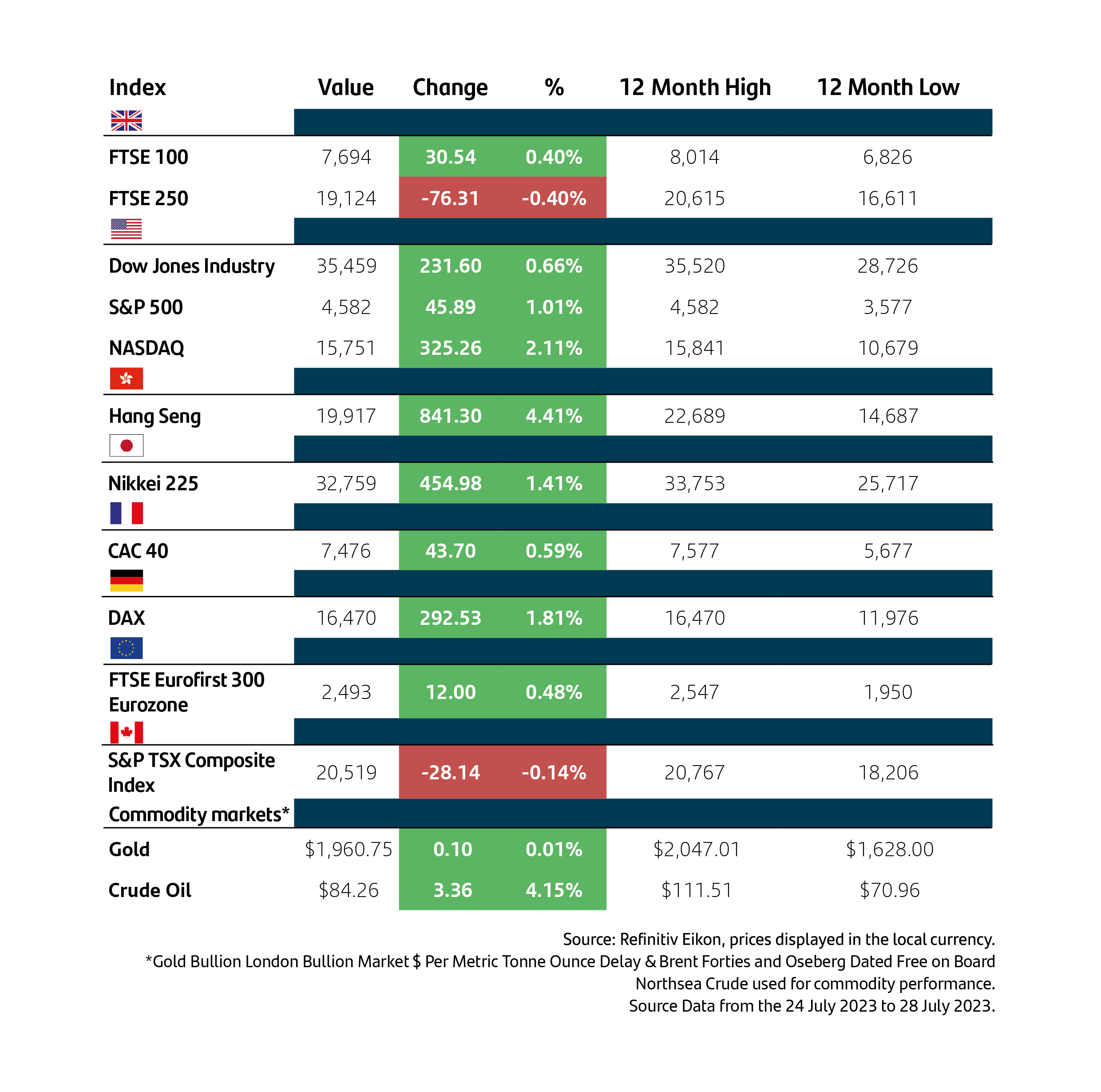

Global stock markets have been performing well in recent weeks and continue to perform well this year. Last week, the S&P 500 was up 1.01% and the NASDAQ was up 2.11%, respectively.3 Earlier in the year, enthusiasm was sparked by the growth of AI (artificial intelligence) and saw the NASDAQ4, which contains 100 of the world’s largest non-financial companies, many of which are major technology companies, gain 37.07% year to date.5 More recently, global stock markets seem to have been lifted by three key points:

• Central banks may be nearing an end to rate hikes.

• Inflation is continuing to moderate.

• Economic growth remains resilient.6

European stock markets have also seen healthy gains recently, last week saw major indices such as the FTSE 100, CAC and Dax up 0.4%, 0.59% and 1.81% respectively.7 In Asia, we saw the Hang Seng index up 4.41% and the Nikkei 225 up 1.41%.8 The result is that 2023 has seen all major stock markets operating in positive territory, giving much-needed relief to investors following the turbulence of 2022.

However, with stock markets performing well this year, some economists are stating that companies are becoming overvalued and that a correction, a market decline that is more than 10%, but less than 20%, might be due in certain markets in order to see companies reflect their true value.9

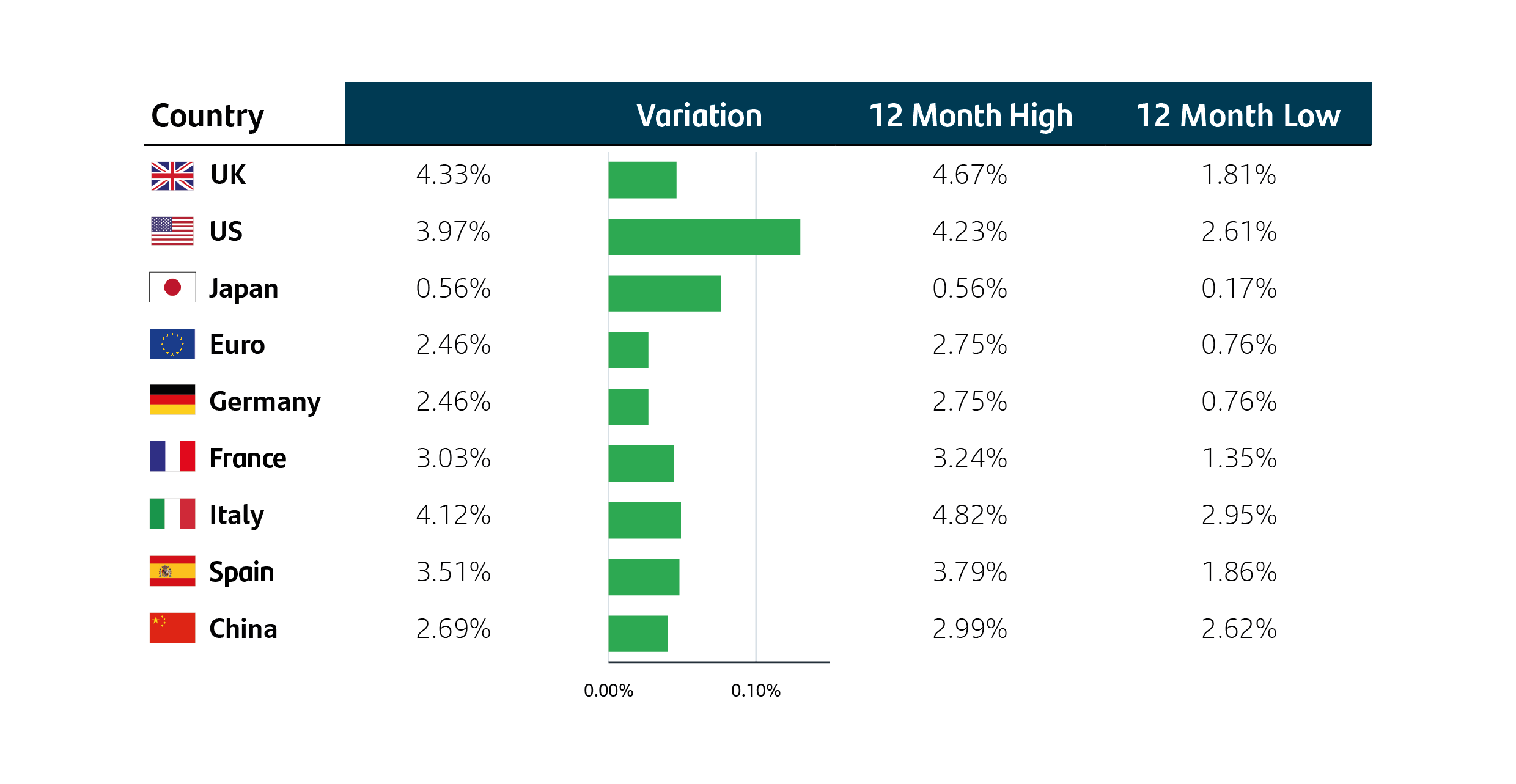

Last week, bonds saw a small increase in yields across all markets, with UK yields up 0.05%, US yields up 0.13% and Europe’s yields up 0.03%.10 However, all markets are below their 12-month highs for yield rates. This reflects the market view that the peak of interest rates may be on the horizon, we may soon see a pause in rate rises before potentially seeing the easing of interest rates in 2024. According to the CME Fedwatch tool, the US futures markets are pricing in a 27.4% chance of another Fed interest rate rise by the end of 2023, compared to a 90.8% chance last week.11

Let’s keep our eyes on that horizon!

The value of seeking guidance and advice

It is important to seek advice and guidance from a professional financial adviser who can help to explain how to build an appropriate financial plan to match your time horizons, financial ambitions, and risk comfort. If you already have a plan in place, or have already invested, it is important to allocate time to review this to ensure this remains on track and appropriate for your needs.

Performance

10-year bond yields

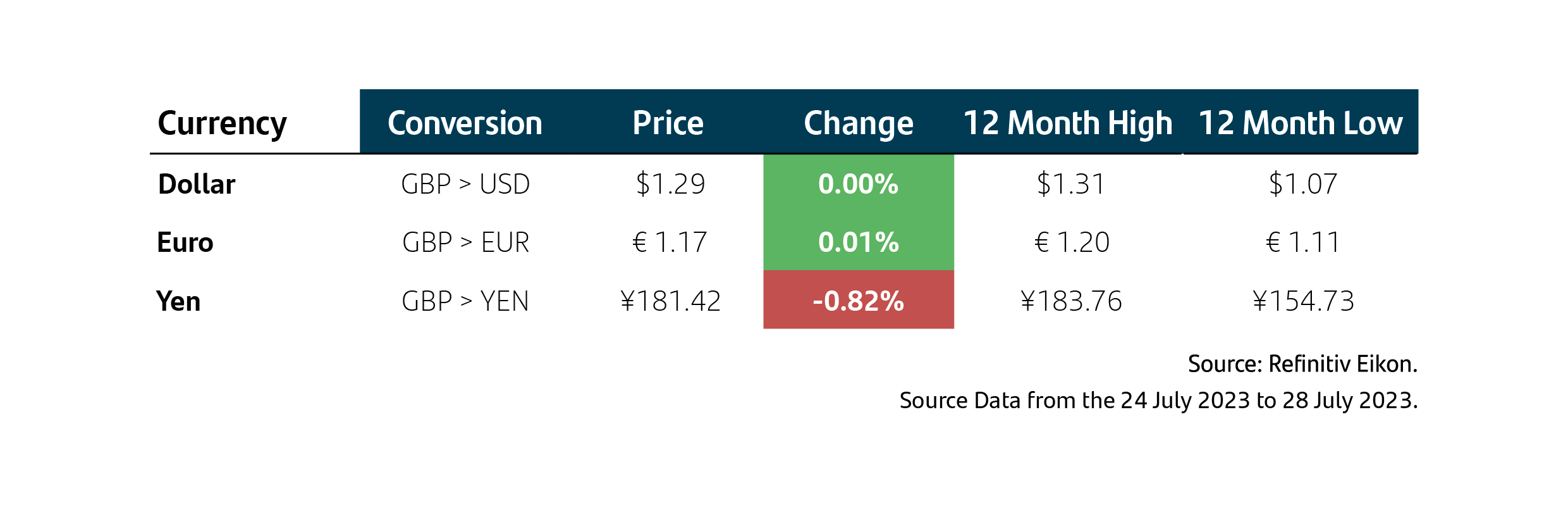

Currencies

Investing can feel complex and overwhelming, but our educational insights can help you cut through the noise. Learn more about the Principles of Investing here.

Note: Data as at 03 August 2023. 1Investing.com, 3 August 2023. 2Bank of England, 3 August 2023. 3Refinitiv Eikon, 31 July 2023. 4Edward Jones, 28 July 2023. 5Market Watch, 31 July 2023. 6Edward Jones, 28 July 2023. 7Refinitiv Eikon, 31 July 2023. 8Refinitiv Eikon, 31 July 2023. 9Yahoo Finance, 23 July 2023. 10Refinitiv Eikon, 31 July 2023. 11T.RowePrice, 28 July 2023.

Important information

For retail distribution.

This document has been approved and issued by Santander Asset Management UK Limited (SAM UK). This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities or other financial instruments, or to provide investment advice or services. Opinions expressed within this document, if any, are current opinions as of the date stated and do not constitute investment or any other advice; the views are subject to change and do not necessarily reflect the views of Santander Asset Management as a whole or any part thereof. While we try and take every care over the information in this document, we cannot accept any responsibility for mistakes and missing information that may be presented.

The value of investments and any income is not guaranteed and can go down as well as up and may be affected by exchange rate fluctuations. This means that an investor may not get back the amount invested. Past performance is not a guide to future performance.

All information is sourced, issued, and approved by Santander Asset Management UK Limited (Company Registration No. SC106669). Registered in Scotland at 287 St Vincent Street, Glasgow G2 5NB, United Kingdom. Authorised and regulated by the FCA. FCA registered number 122491. You can check this on the Financial Services Register by visiting the FCA’s website www.fca.org.uk/register.

Santander and the flame logo are registered trademarks.www.santanderassetmanagement.co.uk