Once again, it’s that time of year when the gardens of the Royal Hospital Chelsea are transformed into the world’s leading floral design spectacle, the RHS Chelsea Flower Show. Next week, leading garden designers will be competing at Chelsea for a coveted RHS Gold medal after months of rigorous planning and the nurturing of green shoots recovering from the rigours of the wet British winter. Is the UK economy showing signs of blooming or is more work needed to remove the weeds? Santander Asset Management UK shares their insights in this week’s State of Play.

Shoots of recovery

The UK economy has also endured the rigours of the British winter, ending 2023 with two consecutive quarters of negative Gross Domestic Product (GDP) leading to a technical recession. This coupled with interest rates being at their highest levels since 2008 at 5.25%, any signs of recovery seemed a faint and distant hope.

Fast forward just four months, winter now feels like a long time ago. Green fingered or not, green shoots of recovery can be found in a stream of recent economic data releases, both in the UK and further afield, not to mention the herbaceous borders adorning the immaculate show gardens of Chelsea.

Economic growth surprise

Last week’s release of UK GDP for Q1 2024 surprised on the upside at 0.6% versus forecasts of 0.4%, the strongest expansion of the UK economy in over two years and ending the technical recession of the second half of 2023.1

Encouragingly, this was the strongest growth for any G7 country (with available data), with 0.3% for the Eurozone and 0.4% for the US over the same periods. However, it must be seen in a broader context. For example, the UK economy has grown by just 1.7% since the fourth quarter of 2019, far less than the 8.7% growth in the US and the 3.4% increase in the Eurozone over the same period2, but nevertheless, any surprise on the upside is to be welcomed.

BoE optimism

As expected last Thursday, the Bank of England’s (BoE) Monetary Policy Committee (MPC) voted 7/2, up from 8/1 at the last MPC meeting, to hold interest rates at 5.25%. While this wasn’t headline worthy news, what the Governor of the BoE, Andrew Bailey, said in the press conference following the announcement was.

For some months now, markets have been playing the ‘when will central banks start cutting interest rates’ game, and by doing so, got somewhat over excited towards the end of 2023 and into the start of 2024, pricing in premature rate cuts contrary to central banks, notably the BoE and the US Federal Reserve’s clear messaging that interest rates would likely remain higher for longer.

So you can imagine the market’s collective sharp intake of breath when Andrew Bailey announced: ‘It is likely we will need to cut bank rates over the coming quarters, possibly more so than currently priced into market rates.’

This unexpected increase in the potential size of future rate cuts by the BoE provides yet more evidence of those elusive green shoots. However, the Governor did add in response to questions on the timing of the first cut that: ‘June cut can neither be ruled out nor a fait accompli’ and ‘there needs to be more evidence that inflation is under control’.3

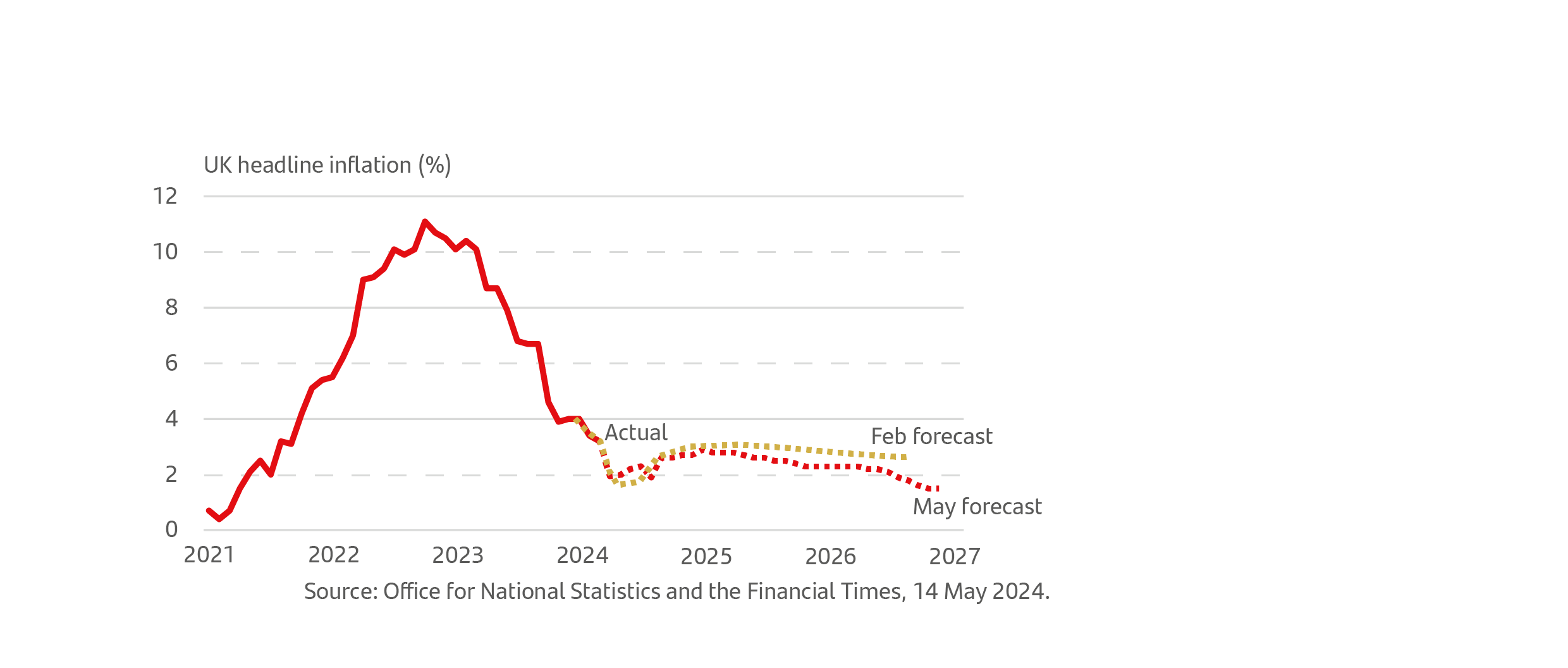

Andrew Bailey continued, stating there was ‘encouraging news’ with the BoE lowering its outlook for inflation over the medium term, as seen in the chart below, and that the BoE’s MPC were confident inflation would fall close to the 2% target in the next couple of months.

The BoE lowered its outlook for inflation over the medium term

Therefore, all eyes will be on the next UK inflation data release scheduled for 22 May. Will this be the set of numbers that finally sees the starting pistol of rate cuts fired?

FTSE 100 - Higher highs

The good news continues, with evidence that those greener shoots are spreading and finally reaching the UK stock market, with the FTSE 100 (the UK’s top 100 companies by market capitalisation) reaching an all-time high closing Friday’s (10 May) session at over 8,400.4

This growth in the FTSE 100 is to be welcomed as it has lagged other developed market indices over the past few years, but with the likelihood of rate cuts hopefully sooner rather than later, a weaker pound versus the dollar and stronger corporate earnings have contributed to a return of 9.15%5 year to date.

Of course, the UK doesn’t operate in isolation, but for once, it is good to pause for a moment and celebrate some positive news.

Watch out for the weeds

There is always one weed to spoil your border and there’s one set of economic data to take the edge of what has been an uplifting set of data so far. That brings us to the recent UK wage growth data, which delivered the 10th consecutive month of real (after the effects of inflation) wage growth. Good news for households, but the 6.0% wage growth excluding bonuses and 5.7% including bonuses translate into real wage growth of 2% and 1.7%, respectively6, which plays to the hawks within the BoE MPC who require further evidence that inflation is under control before voting for interest rate cuts. These figures need to be put in context against a slowing jobs market, with UK unemployment data confirming a slight rise to 4.3%.6 The question for the MPC at their next meeting in June will be whether the rise in unemployment is sufficiently strong to dampen the inflationary effects or real wage growth and leads to increased pressure to cut rates, thereby further stimulating economic growth.

We will have to wait and see. For now, our gardens are blooming, summer is nearly here and there is every reason to remain optimistic.

Good luck to everyone participating in next week’s RHS Chelsea Flower Show, may your blooms be as plentiful as the recent run of economic data.

The value of seeking guidance and advice

It is important to seek advice and guidance from a professional financial adviser who can help to explain how to build an appropriate financial plan to match your time horizons, financial ambitions and risk comfort. If you already have a plan in place or have already invested, it is important to allocate time to review this to ensure this remains on track and appropriate for your needs.

Investing can feel complex and overwhelming, but our educational insights can help you cut through the noise. Learn more about the Principles of Investing here.

Note: Data as at 16 May 2024. 1Office for national Statistics, 10 May 2024, 2Resolution Foundation, 10 May 2024, 3Financial Times, 9 May 2024, 4This is Money, 10 May 2024, 5Morningstar, 14 May 2024, 6Financial Times, 13 May 2024

Important information

For retail distribution.

This document has been approved and issued by Santander Asset Management UK Limited (SAM UK). This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities or other financial instruments, or to provide investment advice or services. Opinions expressed within this document, if any, are current opinions as of the date stated and do not constitute investment or any other advice; the views are subject to change and do not necessarily reflect the views of Santander Asset Management as a whole or any part thereof. While we try and take every care over the information in this document, we cannot accept any responsibility for mistakes and missing information that may be presented.

The value of investments and any income is not guaranteed and can go down as well as up and may be affected by exchange rate fluctuations. This means that an investor may not get back the amount invested. Past performance is not a guide to future performance.

All information is sourced, issued, and approved by Santander Asset Management UK Limited (Company Registration No. SC106669). Registered in Scotland at 287 St Vincent Street, Glasgow G2 5NB, United Kingdom. Authorised and regulated by the FCA. FCA registered number 122491. You can check this on the Financial Services Register by visiting the FCA’s website www.fca.org.uk/register.

Santander and the flame logo are registered trademarks.www.santanderassetmanagement.co.uk