Over the last three years, any new investor might be forgiven for thinking that investing is like riding the fastest rollercoaster at a theme park. However, when you step back and use time to provide perspective, investing becomes a question of appropriate planning. Investing is a long-term part of any financial plan, but how long is long-term? Our Senior Investment Specialist, Simon Durling, shares his thoughts in this week’s State of Play.

Key highlights from this week’s State of Play

- Roller coaster or merry-go-round?

- Wealth calendar

- How long is long-term?

- Market update

Roller coaster or merry-go-round?

Any investor, whether they be a typical retail investor, a professional fund manager, or even those who comment on financial markets, will tell you that investment markets tend to follow a certain cycle directly linked to the changing economic environment. If you have been invested for long enough, you will be aware that when investments seem to gain momentum or when uncertainty grips market sentiment, it can carry you on an eventful ride. It is important for those either looking to invest and are unsure, or those already invested and constantly doubt if they have made the right decision, to acknowledge there are some key ingredients to successful investing. In this week’s update, I want to take some time to explore how to approach investing to protect against some of the pitfalls and avoid buyer’s remorse.

Wealth calendar

Unconventionally, I want you to visualise the calendar you may have pinned on the notice board in your kitchen or office, or perhaps on your fridge, secured by a colourful magnet. Many of us no doubt lead very busy lives centred around the time we spend at home, at work or at play. I would argue most calendars, like mine at home, cover the current calendar month, which is run by my wife, has five columns, offering each person in the home the opportunity to write up-and-coming events, appointments, or work shifts. I must admit, I struggle to get into the habit of updating this (much to my wife’s annoyance), as I am guided by my work diary for obvious reasons.

If you take the visual of what I have just described and stretch the calendar over different time frames, then you can start to think through what to populate this with and, importantly, why. The reason this becomes so important is that you can break down your wealth and segment it into different pots or buckets. By doing this effectively, you can hit the sweet spot of effective financial planning: having the right money, in the right product, over the right time frame, and crucially, for the right reason. Let’s explore the long-term bucket.

How long is long-term?

Many retail savers looking to invest for the first-time struggle with longer-term time horizons. Often, this is because they see investments as untouchable or inflexible, when in fact they are usually the opposite. Clearly, the initial guidance is to think of a minimum term of 5 years. This is because investment values can go down as well as up, and you may not get back the amount you invested (the normal disclaimer on any investment product or solution).However, while investment values vary every day, to ensure you are not forced to sell part or all of your investment at the wrong time, five years is the minimum threshold (in fact, nearly all underlying investments, whether this be bonds or shares, change all the time during the trading day).

Statistically, I would argue that, given what has happened in the last 3 years, for most to avoid being forced to sell investments at the wrong time and suffer unnecessary losses, many investors may be more comfortable investing over much longer time frames. Designing and putting in place an investment portfolio to match your time horizons and risk appetite helps ensure there are no nasty surprises. However, depending on when you invest, as your life changes and you get older, your investment portfolio can be changed and adapted over time to match these changing needs.

It is not just retirement income that may be required. Maybe you have plans to pass on some or all your wealth to your family. You may need to utilise your savings and investments to top up your retirement income, especially in the early years of retirement when, hopefully, better health enables you to work through your long-held ambitions, dreams, or bucket list. Because most investment solutions are open-ended and few have exit penalties (apart from market timing), it enables you to use this wealth pot for various goals over varied timeframes.

Importantly, whether we like it or not, the wealth we accumulate during our working lives may need to last us for as long as we live to ensure we widen our choices. Investments reward patience, so let’s look at what history tells us.

What history tells us

When times of crisis come, no-one can know what the long-term outcomes will be. What we do know, however, is that over the long-term it’s generally better to stay invested through the downs as well as the ups. Over time, investment market growth tends to balance out the short-term ups and downs.

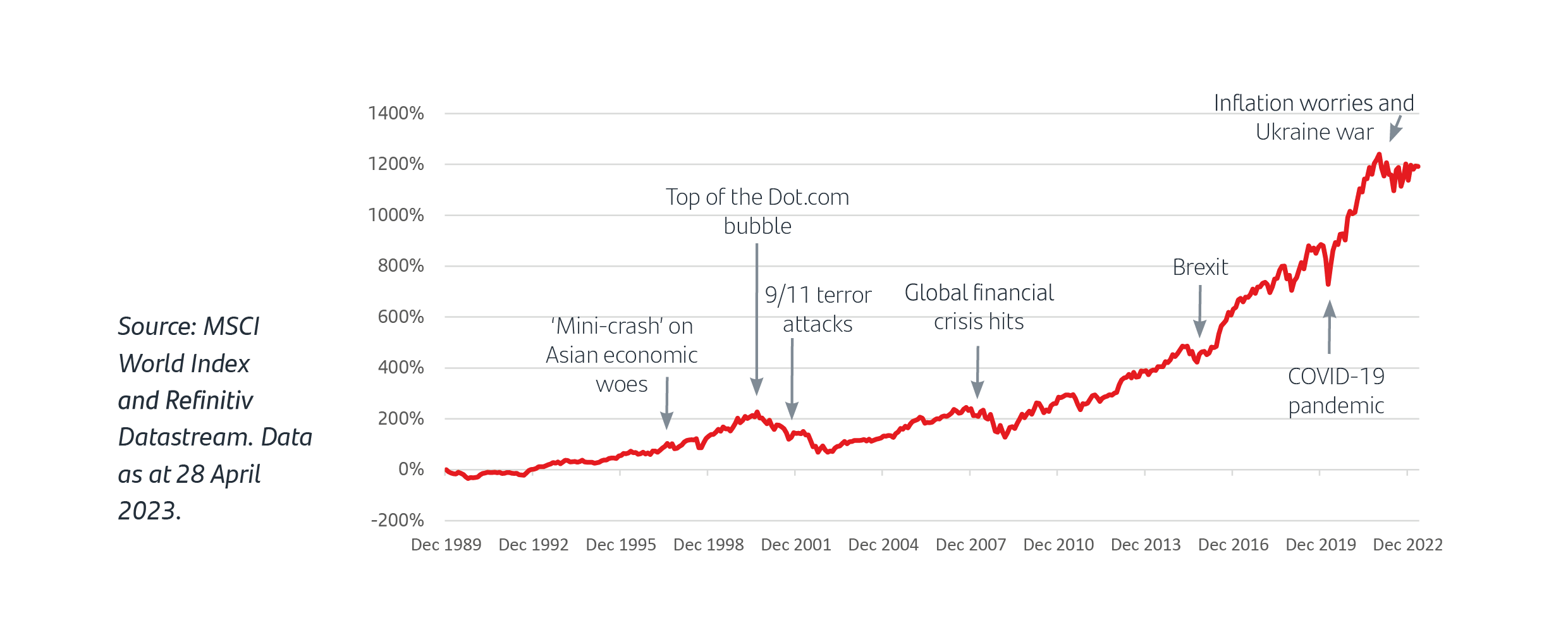

This chart shows the performance of the MSCI World Index since January 1990 with some key events highlighted.

Whilst past performance is not a guide to future performance and investment returns will depend on when you invest and when you take your money out again, in almost all cases a downturn is followed by growth. Over the longer-term, the general trend is an upward one.

Understanding your instincts

Looking at the data like this is very different to watching the impact on your own investments. And when emotions run high it can be tempting to make short-term decisions in response, which you could later regret.

You’re only human

Research by behavioural psychologists has shown that investors tend to feel the pain of losses more keenly than the pleasure of equal gains. That might lead you to sell in a falling market and make your losses real.

Another very human trait is to do what everyone else is. That might lead you to put money into investments with already high prices, driven up by demand, and that rationally offer little room for further growth.

Do I need to take action?

Remember, your investment goals and objectives may change so reviewing your portfolio regularly is a good idea. It often pays to ignore short-term noise and uncertainty, stick with it and keep focused on your investment goals. But, of course, there are exceptions. If you’re unsure about investing or worried about your investment portfolio, a financial adviser can help you weigh everything up, based on your own personal circumstances, and make the right decisions for you.

Market update

Investment markets have been searching for direction for many weeks. While this year’s investment values are broadly up since the start of the year, this has been overshadowed by volatility, making the journey quite bumpy at times. Now, investors seek clarity amid the uncertainty. Central banks have continued to increase interest rates as economies have performed better than expected and avoided the recessions predicted by policymakers and economists. All eyes turn to the next round of rate meetings, monitoring the latest data on unemployment and inflation. Most central banks need to see the data start to show that interest rate rises are starting to slow their respective economies before they press the pause button.

Last week’s US inflation data was broadly in line with expectation, and core inflation continues to fall but all too slowly to suggest that the inflation battle has yet been won. The Bank of England suggested last week that they would keep a close eye on the data (UK inflation data is due next Wednesday) before June’s Monetary Policy Committee Meeting to decide on whether to add to last week’s 0.25% rise.1 As I have mentioned many times in previous updates, interest rate rises are a blunt tool that take at least 6 months, often 12 months, to really impact consumption. The other important factor weighing on the Federal Reserve in the US will be the level of confidence in the banking sector. The recent crisis will likely have tightened up credit availability, meaning a potential drag on future economic output, the equivalent of a rise in interest rates. If they raise rates too far, the consequences could be that the economy slows much further than desired impacting future growth prospects.

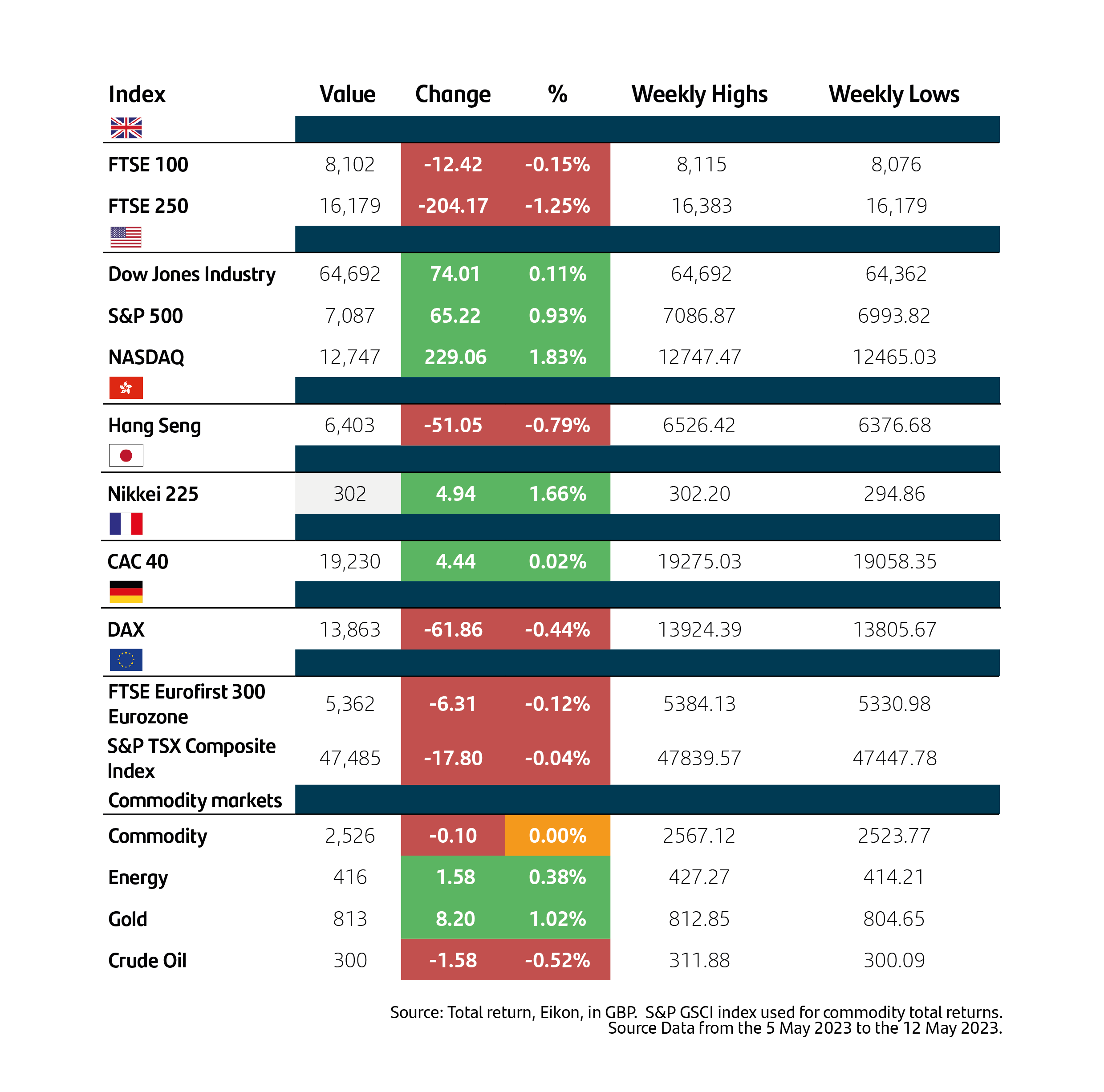

Santander Asset Management UK receives regular feedback about the content of State of Play, and where possible, we try to accommodate suggestions. This week’s update, for the first time, will show market data reflecting a wide range of share indices, bond yields, currencies and commodities. It is intended only as reference point to help readers compare the narrative with market values looking back at the previous trading week. This captures data at the close of business on the preceding Friday and compares it with the change from the previous trading week. The data is sourced by Santander Asset Management UK’s investment team using Eikon.

A week in the markets

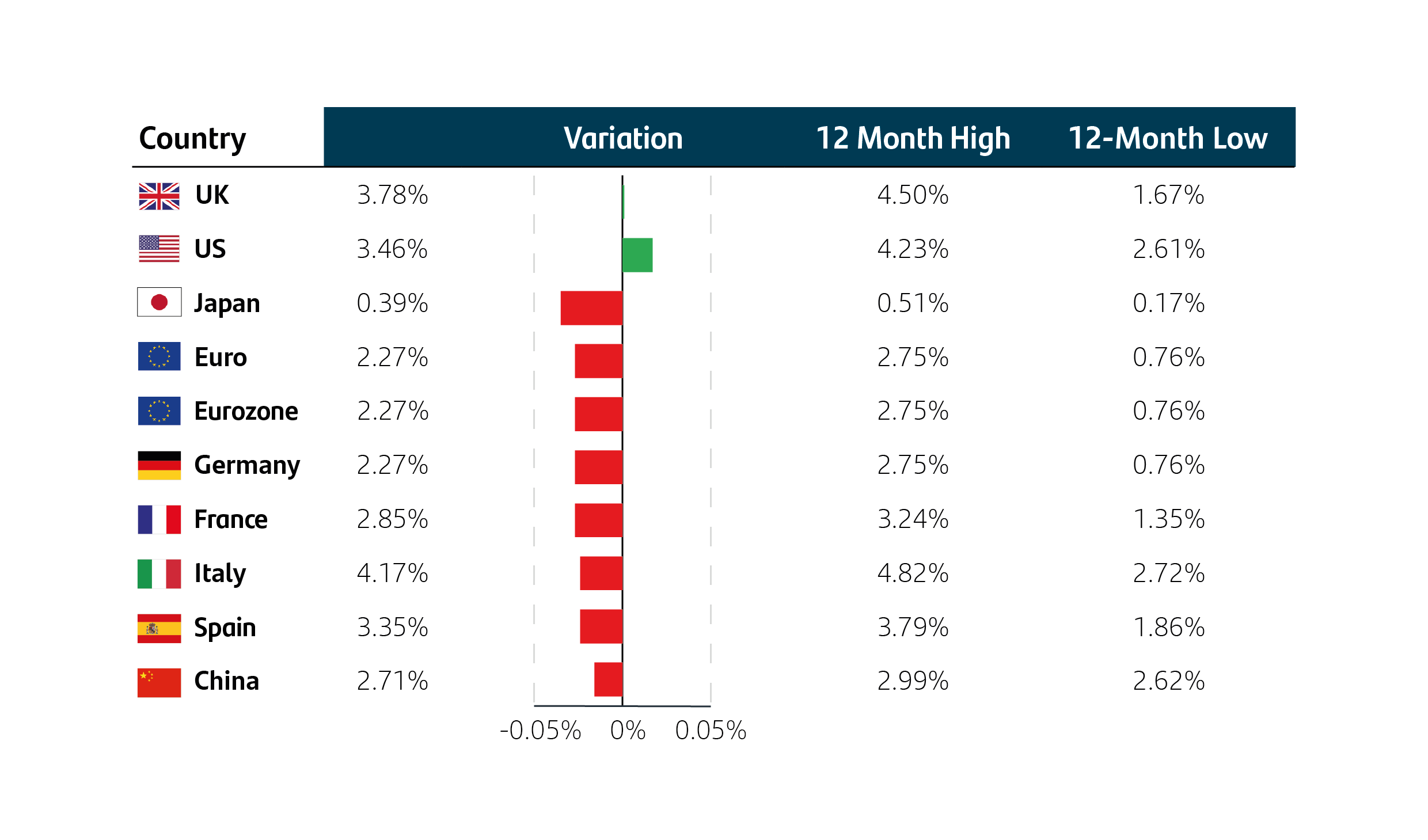

Performance 10-year bond yields

10-year bond yields Currencies

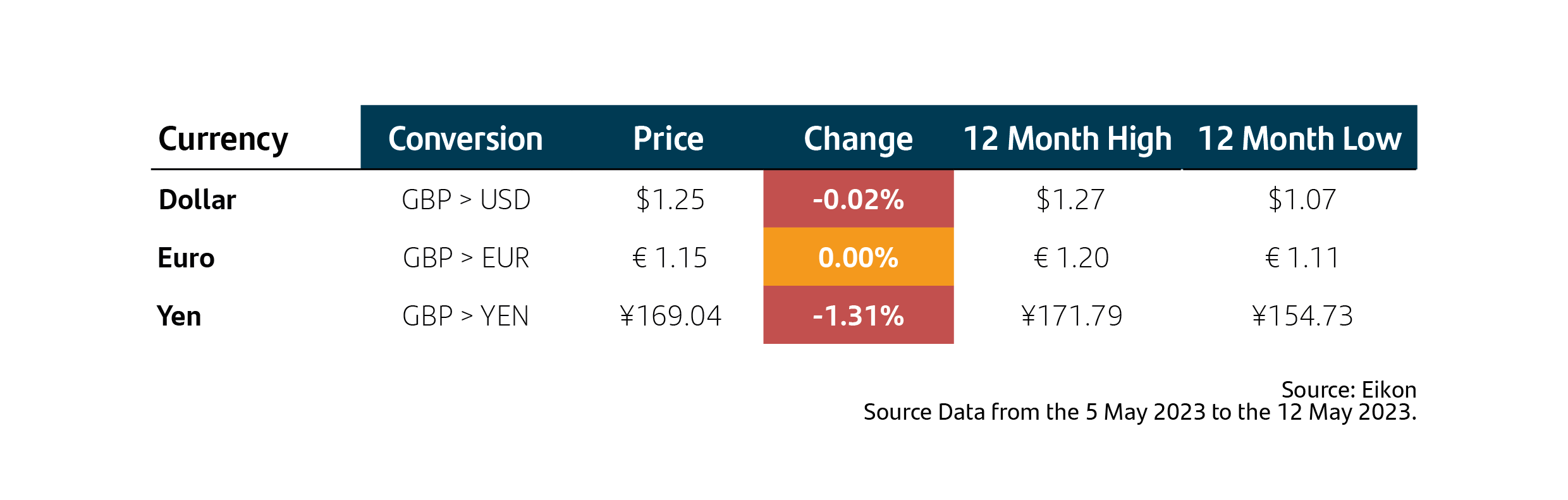

Currencies

Investing can feel complex and overwhelming, but our educational insights can help you cut through the noise. Learn more about the Principles of Investing here.

Note: Data as at 18 May 2023. 1Bank of England, 16 May 2023.

Important information

For retail distribution. This document has been approved and issued by Santander Asset Management UK Limited (SAM UK). This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities or other financial instruments, or to provide investment advice or services. Opinions expressed within this document, if any, are current opinions as of the date stated and do not constitute investment or any other advice; the views are subject to change and do not necessarily reflect the views of Santander Asset Management as a whole or any part thereof. While we try and take every care over the information in this document, we cannot accept any responsibility for mistakes and missing information that may be presented.

All information is sourced, issued and approved by Santander Asset Management UK Limited (Company Registration No. SC106669). Registered in Scotland at 287 St Vincent Street, Glasgow G2 5NB, United Kingdom. Authorised and regulated by the FCA. FCA registered number 122491. You can check this on the Financial Services Register by visiting the FCA’s website www.fca.org.uk/register