Investing an appropriate share of your investment portfolio into bonds (also known as fixed income) to match your risk comfort has been a guiding principle for decades. Offering the potential to diversify your portfolio to smooth the long-term ride, bonds experienced a golden journey known as the ‘bond bull market’. However, for bond investors, last year was the worst since records began as interest rates soared and bond values plummeted. So, what does the future now hold for bond investors? Our Senior Investment Specialist, Simon Durling, shares his thoughts in this week’s State of Play.

Key highlights from this week’s State of Play

- Back to basics - bonds

- End of bond bull market

- Better days ahead?

- Market update

Back to basics: What is a bond? (Fixed income)

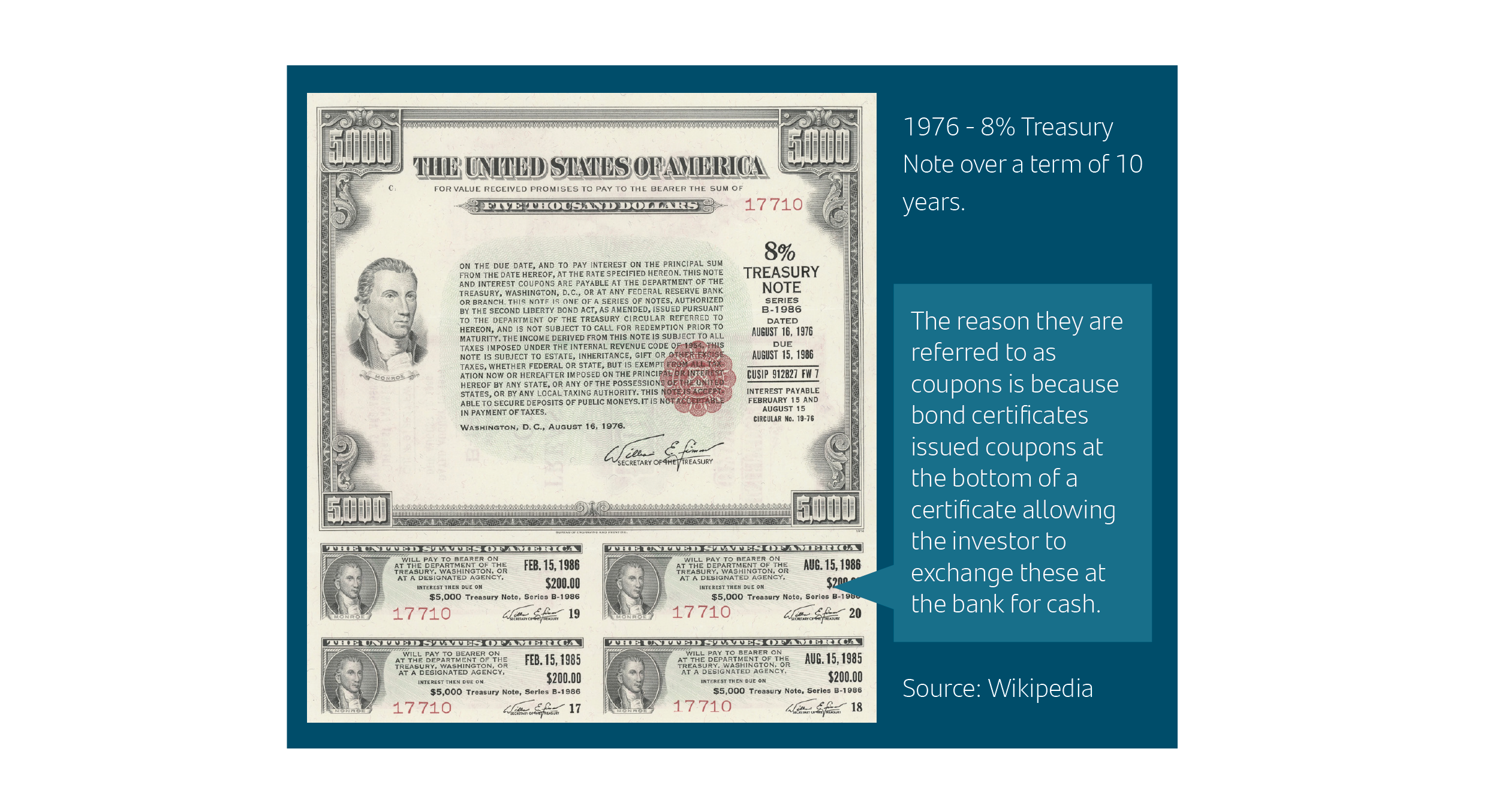

Bonds are very similar to I owe you’s (a debt). The investor lends money, typically to either a country or a company, for a fixed period in return for interest. The money the investor lends is known as the principal, or face value, and over the term of the bond, they receive regular interest payments, called coupons. These coupons are fixed throughout the term of the loan, hence why these assets are known as ‘fixed income’ assets. Assuming the company or institution doesn’t go bust, at the end of the agreed period, the investor is paid back the money they are owed. The debt itself may be bought when it is issued or more commonly in the secondary market, which enables investors to buy and sell existing debt, where the value of the principal will change based on a few important factors. In addition, if the bond is purchased, either at issue or after, it is not necessary for the investor to hold the bond until maturity, as they can ‘sell’ the debt to another investor before the maturity date.

US government bond

Why do companies raise money using bonds?

A sensible question that may be asked is: ‘Why doesn’t a company just borrow the money from a bank?’ Depending on economic conditions and the outlook, approaching commercial banks to borrow money may be the best solution for companies looking to borrow or ‘raise’ capital. Another solution is to ‘sell’ a portion of the company’s value by issuing shares for investors to buy (think Dragons Den). However, depending on market conditions and the market’s appetite for buying corporate debt, the same company may be able to issue a bond over the right timeframe at a lower interest rate, lowering the cost of borrowing. Normally, the bond covenants or rules will ensure investors ‘lending’ the money via the bond issue will be ‘first’ in line for any assets in the event of a company going bust, and importantly, before ordinary shareholders.

Source: Investopedia

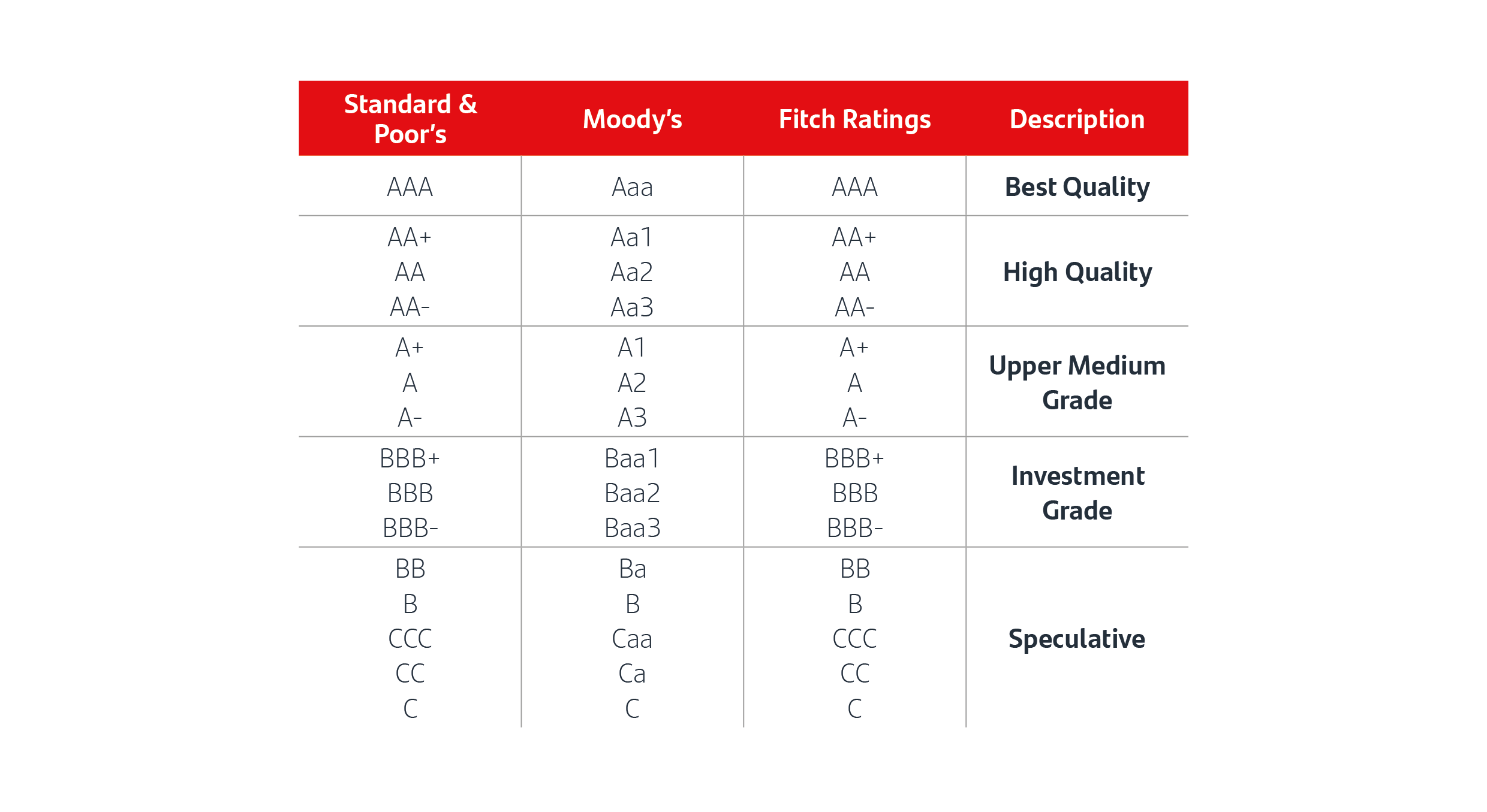

Regardless of whether a country, a company, or an organisation is borrowing money when issuing a new bond, the amount of the interest rate or coupon is typically determined by two key elements: the term of the bond and the risk of default. The ‘credit worthiness’ is normally built around a rating given by different ‘rating agencies’ like Standard and Poor’s or Moody’s. Like consumers, governments and companies are assigned a credit score based on their ability to meet their financial commitments. Interest payments are usually highest on bonds with the lowest credit ratings because they are perceived to be a greater risk for investors.

‘Credit ratings are forward looking opinions about an issuer’s relative creditworthiness. They provide a common and transparent global language for investors to form a view on and compare the relative likelihood of whether an issuer may repay its debts on time and in full. Credit Ratings are just one of many inputs that investors and other market participants can consider as part of their decision-making processes.’

Source: Standard & Poor’s

When a bond has a high rating – anything from ‘AAA’ down to ‘BBB’ – they are deemed to be ‘investment-grade’, lower-risk bonds. On the corporate side, these ratings are usually given to financially robust institutions, such as utility companies and supermarkets. Anything below this rating is considered ‘sub-investment grade’, as the risk of default on the debt being issued is much higher. Over the years, the choice of bonds has expanded extensively, including high-yielding overseas bonds and emerging market bonds, often from large companies with excellent balance sheets, which offer better coupons than traditional corporate debt.1

The difference between interest rate and yield?

When a new bond is issued, the interest rate or coupon being paid is normally fixed. If the investor buys the bond at issue, then the yield and the interest rate being paid are the same, assuming the bond is held all the way through to maturity. However, most bonds are bought and sold through a secondary market, and the principal value based on a starting value of £100 will change depending on any changes to the interest rate environment and outlook or the financial wellbeing of the issuer of the bond in question. Bond prices will rise when interest rates fall because the rates of interest they pay are fixed and may beat the short-term rates available from banks. Therefore, you may buy a bond or a UK Government bond for an amount above or below the nominal value, and this will have an impact on both how much interest you receive as an income and the amount of money you will receive when the bond matures.

Yield is a general term that relates to the return on the capital you invest in a bond. The yield of a bond reflects the price you paid for the principal in relation to the fixed income being paid to maturity. So, as a simple example, if the bond costs £110 and pays 4% through to maturity, while the 4% is fixed, the bond will cost more than the original £100 issue price. The interest rate being paid of 4% divided by the purchase price of £110 means the yield is 3.63%, not the 4% fixed income. Conversely, if you bought the same bond for £90, the yield would be much higher at 4.44%. A bond’s price and yield determine its value in the secondary market.

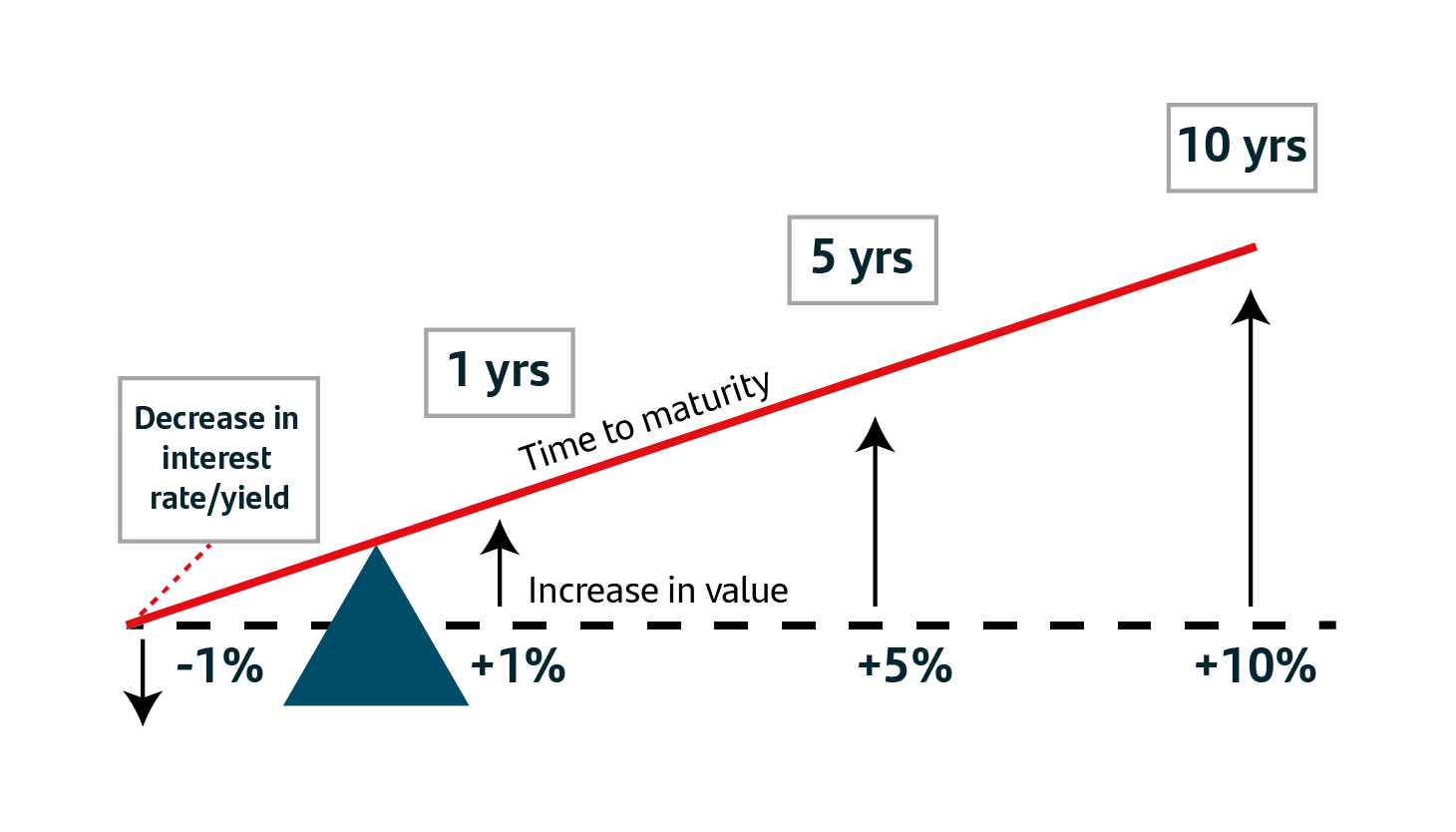

The duration seesaw

There is an inverse relationship between the price and the yield of a bond. Another important factor is knowing how much a bond’s value will increase or decrease when yields rise or fall. Putting aside a change in default risk, to estimate how sensitive a particular bond’s value is to interest rate and yield movements, bond investors use a measure known as duration. In 1938, economist Frederick Macaulay suggested duration as a way of determining the price volatility of bonds. ‘Macaulay duration’ was the first method to measure sensitivity to interest rates, but others, like the modified duration calculation (which uses Macaulay’s in the calculation), are also commonly used. Duration can help investors predict the likely change in the price of a bond given a change in the bond yield. Let’s first look at how bond prices are affected if interest rates/yields begin to fall. A concept like duration is very difficult to explain in a way that is easily understood by a retail investor. As you know, State of Play has on many occasions attempted to translate difficult subjects using analogies or examples to help with general understanding. On the next page, we look at how bond prices are affected by changes in yield.

Impact of falling interest rates/yields

Important – this represents a simplified explanation of duration and in practice is always slightly different depending on economic circumstances – it is a guide only.

If we take a simple fall in yield of 1%, which may be a direct result of the Bank of England, or another central bank decreasing interest rates, or it may be because new economic data changes the opinion of bond investors about the future path of interest rates. In the diagram above is a simple seesaw. On the left-hand side is a fall of 1% in the bond yield. If the bond has only 1 year to maturity, then the likely rise in values would be 1%. However, if the time to maturity is 5 years, then the value would increase by 5%. Demonstrating the importance of time, the sensitivity increases, if the time to maturity was 10 years, as the bond value would increase by 10% based on the same 1% decrease in yield. A concept like duration is very difficult to explain in a way that is easily understood by a retail investor. As you know, State of Play has on many occasions attempted to translate difficult subjects using analogies or examples to help with general understanding. Below, we look at how bond prices are affected by changes in yield.

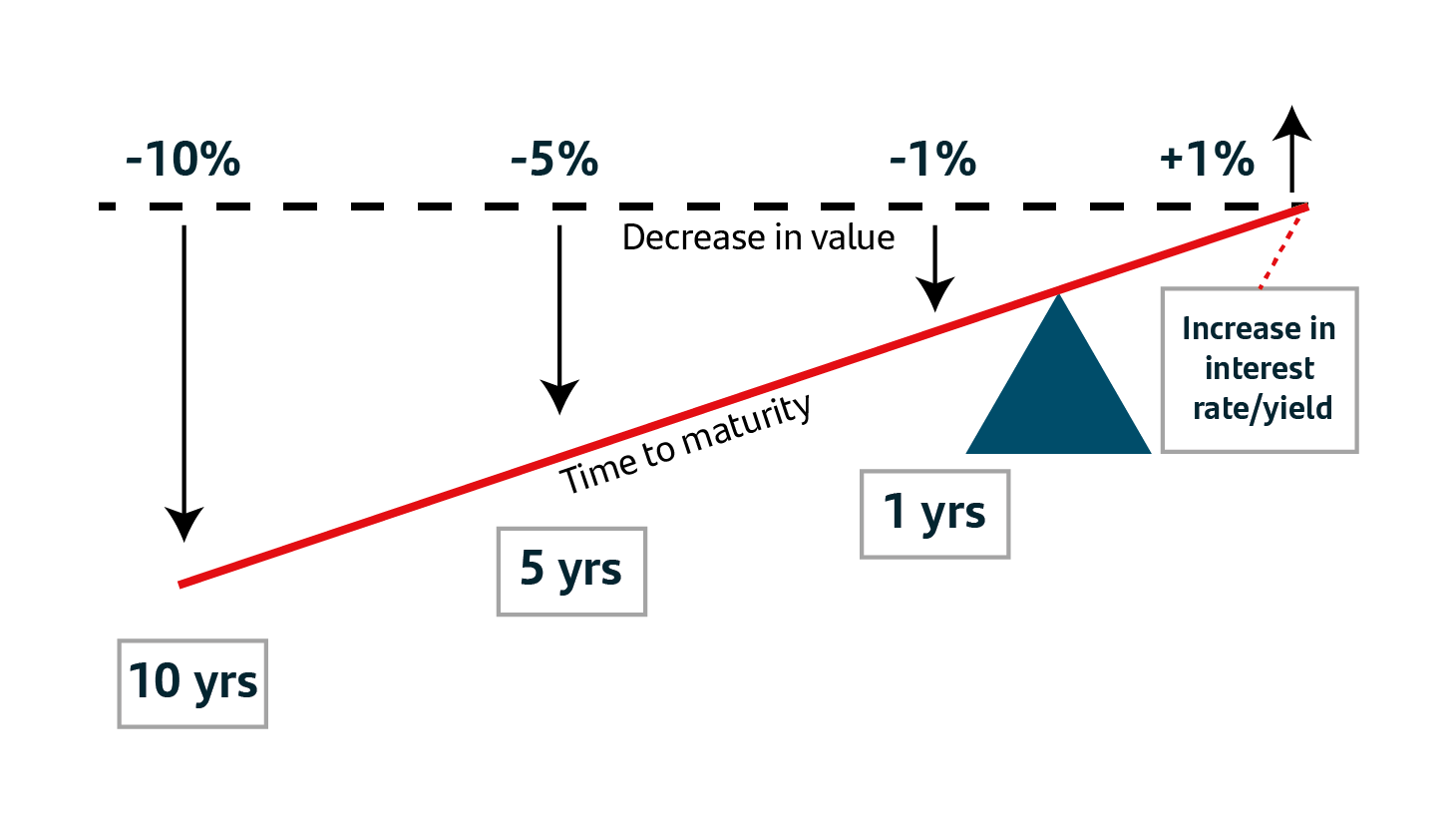

Impact of rising interest rates/yields

Important – this represents a simplified explanation of duration and in practice is always slightly different depending economic circumstances – it is a guide only.

If we then reverse this situation and show how the bond value changes as interest rates/yield increase, you can see a mirrored alternative outcome. Depending on the time to maturity, the bond price falls further when interest rates/yields increase the longer the time to maturity. So, in summary, the longer a bond’s maturity, the longer its duration, because it takes more time to receive full payment and vice versa for short duration. Duration, like the maturity of the bond, is expressed in years, but is typically less than the maturity. While bond investing is generally less risky than investing in shares, factors like duration become important considerations if you decide to sell a bond or bond-type investment before its maturity date.

Below is a simple table to show how yields affect the £100 value of a bond depending on the term.

Important – this represents a simplified explanation of duration and in practice is always slightly different depending economic circumstances – it is a guide only.

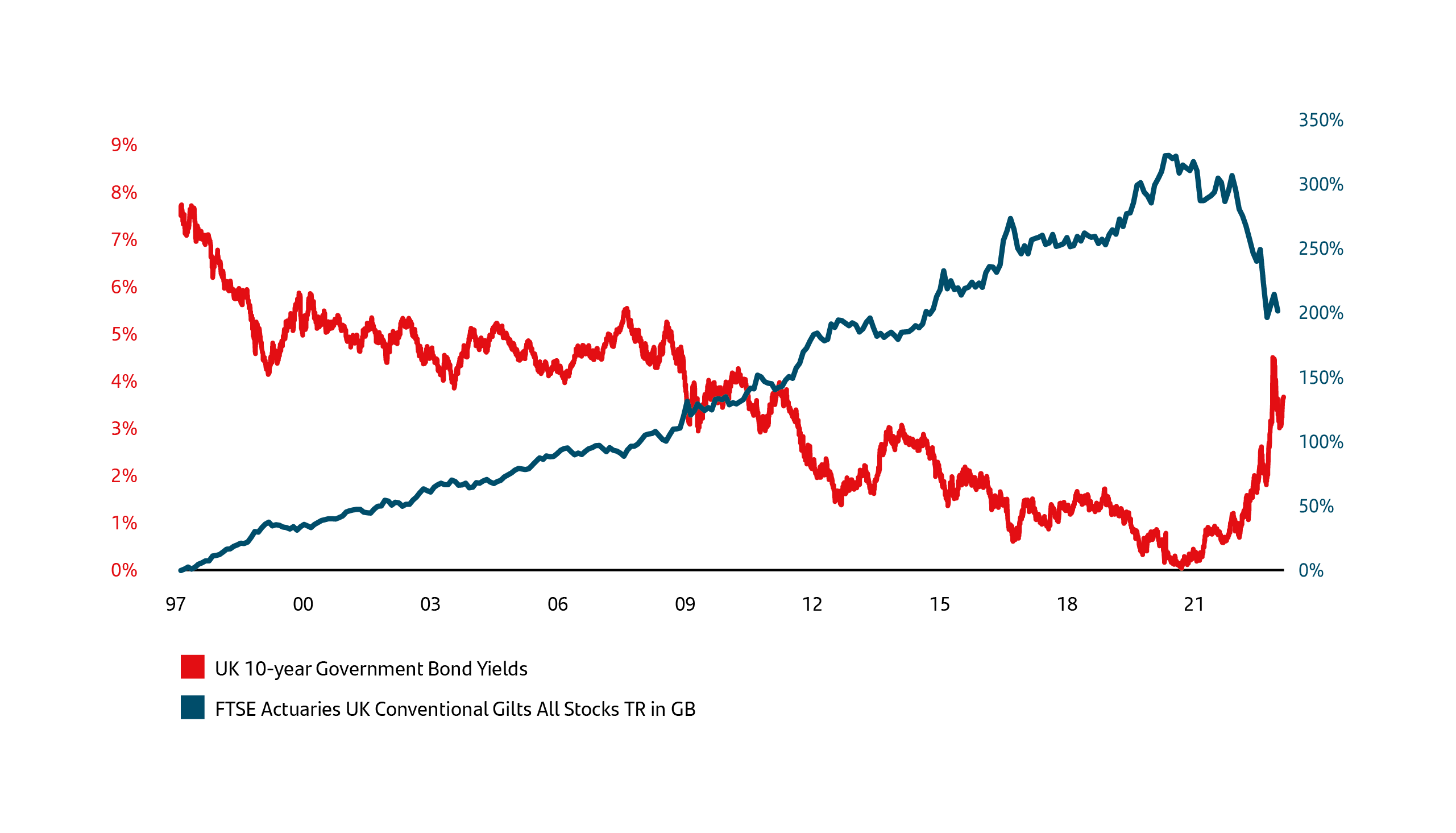

End of the bond bull market

Since the early 1980’s, bond investors have seen yields fall gradually over time until the financial crisis in 2008, when central banks responded with ultra-low interest rates and a vast programme of quantitative easing, where new money was printed on an unprecedented scale. During this time, bond investors have benefited from competitive levels of income and capital gains as yields fell. A reflection of this is shown in the lowest-risk bond investment for UK investors – UK Gilts. If we measure 10-year UK Government bonds between January 1997 and May 2020, which delivered a total return (coupons paid and capital growth) of 325%.2 At the beginning of this period, yields were 8.75% (although yields went as high as 15% during 1981) before falling to 0.1% at the start of July 2020.2 Since 1981, the beginning of the ‘bond bull run’, yields have fallen consistently sending bond values higher and adding to the income received from coupons (interest payments).

Bond bull run comes to an end

Source: Refinitiv Datastream. Data as at 14 October 2022

The risk to bond investors after such a sustained and long bull market was that eventually interest rates were likely to normalise as quantitative easing and low interest rates came to an end. What wasn’t anticipated, especially by central banks, was the rapid return of much higher inflation after the pandemic and restrictions ended. A complex mix of higher pent-up demand, supply chain issues and the conflict in Ukraine, sent prices soaring to a 40-year high.3 The delayed response by central banks prompted an unprecedented and sustained period of rising interest rates. The consequence for bond investors was that the value fell significantly. In late autumn of last year, UK Gilts and UK Corporate Bonds had fallen over 30% in just 12 months, undoing three-quarters of the price rise in bonds over the previous 30 years.2 Since then, yields have fallen and then risen once again, but what can investors expect on the road ahead?

Are better days ahead for bonds?

As with all investment assets, whether this be shares, bonds, property, or commodities, the price you pay and the timing, relative to the market cycle, are crucial. As we have explored on numerous occasions, with shares, the longer you invest, provided this is in a diversified portfolio, the greater the probability of an improved return. Patience and an appropriate portfolio matched to your time horizon, aspirations and risk comfort normally lead to better outcomes. Bond investing and the outlook for bond investors are probably more defined by your entry point and the economic outlook, especially the future path of interest rates. Because a typical bond has a fixed income and a fixed maturity date, neither of these two elements tend to change while they form part of your investment portfolio. (Excluding non-dated bonds and indexed/inflation-linked bonds).

This means it is possible to understand, certainly in the short term, what the prospects for investors might be with a degree of confidence. Clearly, events and economic outcomes can still spring a major surprise and dilute this confidence. At present, headline inflation in most major economies is beginning to fall and expectations for price rises to ease closer to the long-term target of 2%. Market participants are already assessing whether the Federal Reserve may pause rate rises when they meet next month, although this probability has lessened in the last couple of weeks.

In the UK, the prospects look slightly different. Last week’s headline inflation numbers fell sharply, albeit not by as much as had been forecast. The challenge for the Bank of England is their concern about wage settlements and core inflation, which excludes energy and food and is still rising. At present, the market is pricing in further rate rises at the 22 June MPC meeting and at subsequent meetings later this year, with the ‘terminal’ rate (the rate at which rates may stop rising) being estimated at 5-5.25%. However, investors tend to look to the future when pricing in their expectations, which is why a few months ago bond yields fell. The 10-year UK Gilt Yield fell to just over 3% at the end of January as market participants hoped inflation had peaked and central banks were close to pausing rate rises. Yields have subsequently risen as inflation remained stubborn and economic demand remained robust, alongside higher wage settlements than policymakers would have preferred.

I suppose the million-dollar question is: have yields peaked? Is now a good time to invest in bonds? Clearly, it is impossible to answer these questions with any confidence, especially given what we have experienced over the last few years. However, with inflation heading in the right direction and economies set to cool in the next few months, policymakers hope to be able to pause rate rises very soon. In the event this happens, then bond yields should, in theory, start to ease. In the short term, yields may rise further, but it is hard to see them increasing much more from here. Government bonds offer income at over 4%, corporate bonds at over 5% and higher-risk, higher yielding bonds closer to double digits.2 If yields do eventually begin to fall because bond values are inversely related to yields, (i.e higher yields mean lower values and vice versa) then investors benefit from both competitive income and the potential for increased capital values. It is impossible to predict with any certainty when central banks will start to cut interest rates, but with inflation falling and the effects of a sustained increase in interest rates beginning to impact economic demand, experts expect the interest rate pivot to begin next year. I will wait and see with interest to see how things unfold.

Market update

Markets remain nervous despite President Joe Biden and Republican House Speaker Kevin McCarthy reaching a deal in principle over the bank holiday weekend to raise the US debt ceiling. McCarthy faces a revolt from the right wing of his party, furious that the initial deal dilutes their initial demands about cutting spending. McCarthy defended the pact ahead of a vote expected on Wednesday in the House of Representatives (the equivalent of our own House of Commons). Speaking to Fox News, he said, “Maybe it doesn’t do everything for everyone. But this is a step in the right direction that no one thought we would be at today. This is a good bill for the American public.”4

US Treasury Secretary, Janet Yellen, has warned that the US would run out of cash on 5 June unless an agreement can be reached. The agreement raises the debt ceiling until 2025 and sets caps on non-defence spending for the next two fiscal years while allowing the government budget to grow slightly as planned by Biden. It remains to be seen (as the vote happens after the publishing deadline for this week’s update) whether both the President and McCarthy can pacify their respective parties to harness enough votes to avoid financial turmoil.5

The value of seeking guidance and advice

It is important to seek advice and guidance from a professional financial adviser who can help to explain how to build an appropriate financial plan to match your time horizons, financial ambitions, and risk comfort. If you already have a plan in place, or have already invested, it is important to allocate time to review this to ensure this remains on track and appropriate for your needs.

Performance

10-year bond yields

Currencies

Investing can feel complex and overwhelming, but our educational insights can help you cut through the noise. Learn more about the Principles of Investing here.

Important information

For retail distribution. This document has been approved and issued by Santander Asset Management UK Limited (SAM UK). This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities or other financial instruments, or to provide investment advice or services. Opinions expressed within this document, if any, are current opinions as of the date stated and do not constitute investment or any other advice; the views are subject to change and do not necessarily reflect the views of Santander Asset Management as a whole or any part thereof. While we try and take every care over the information in this document, we cannot accept any responsibility for mistakes and missing information that may be presented.

All information is sourced, issued and approved by Santander Asset Management UK Limited (Company Registration No. SC106669). Registered in Scotland at 287 St Vincent Street, Glasgow G2 5NB, United Kingdom. Authorised and regulated by the FCA. FCA registered number 122491. You can check this on the Financial Services Register by visiting the FCA’s website www.fca.org.uk/register