Q3 2024

This publication aims to provide an insight into the changing economic environment and importantly, how this has impacted financial markets and investments. Our Multi-Asset Solutions team at Santander Asset Management UK share their thoughts on the market outlook and how they have adapted investment portfolios to position our clients for the road ahead.

Summary of Quarterly Perspectives content:

- Review of the third quarter of 2024

- Investment performance of different asset classes

- Our expert’s opinion on the investment outlook

- How have our multi-asset fund managers changed their portfolio positioning based on the outlook and our tactical asset allocation

- Summary of the quarterly perspectives

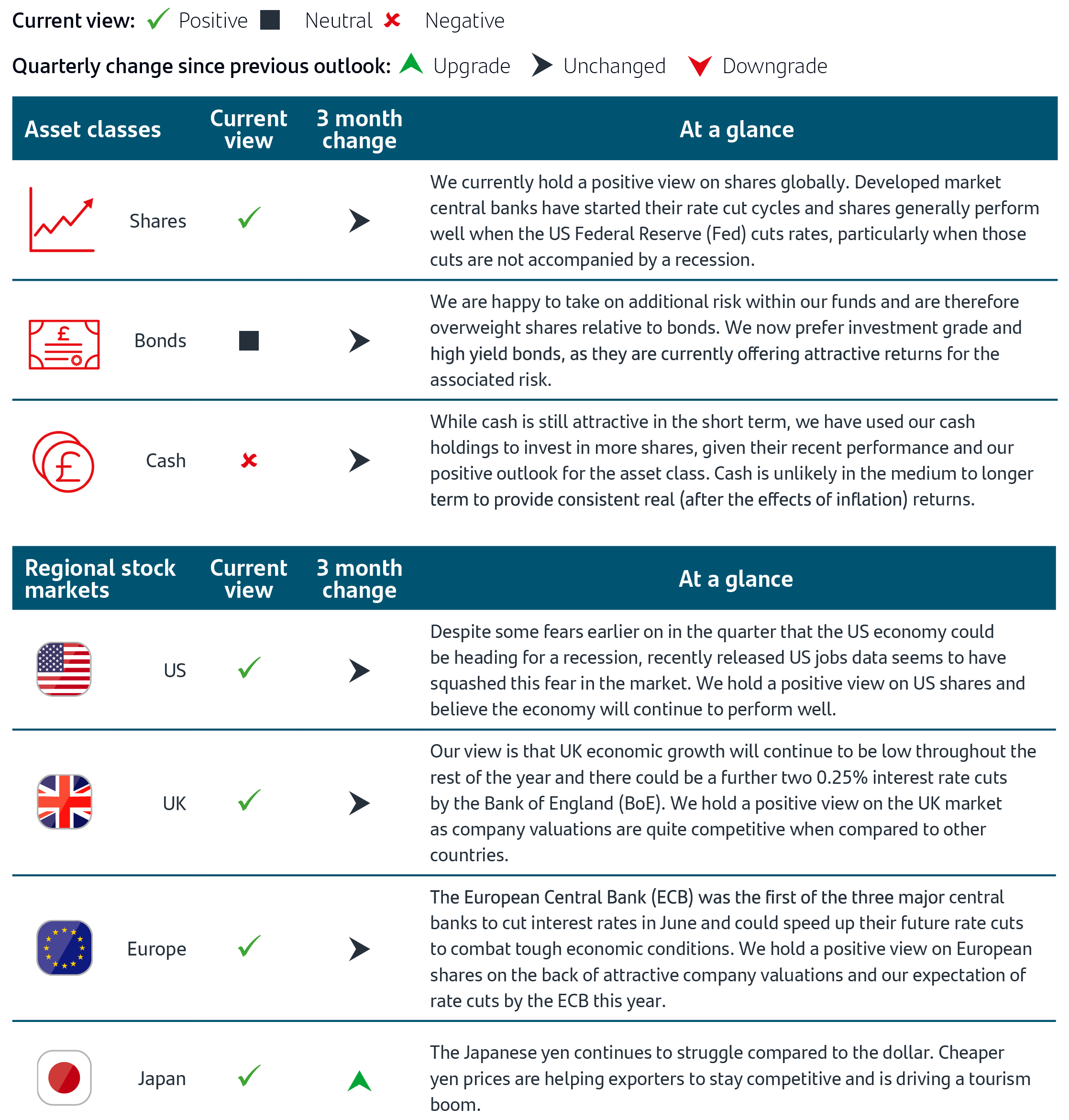

Outlook at a glance

Reviewing the third quarter of the year

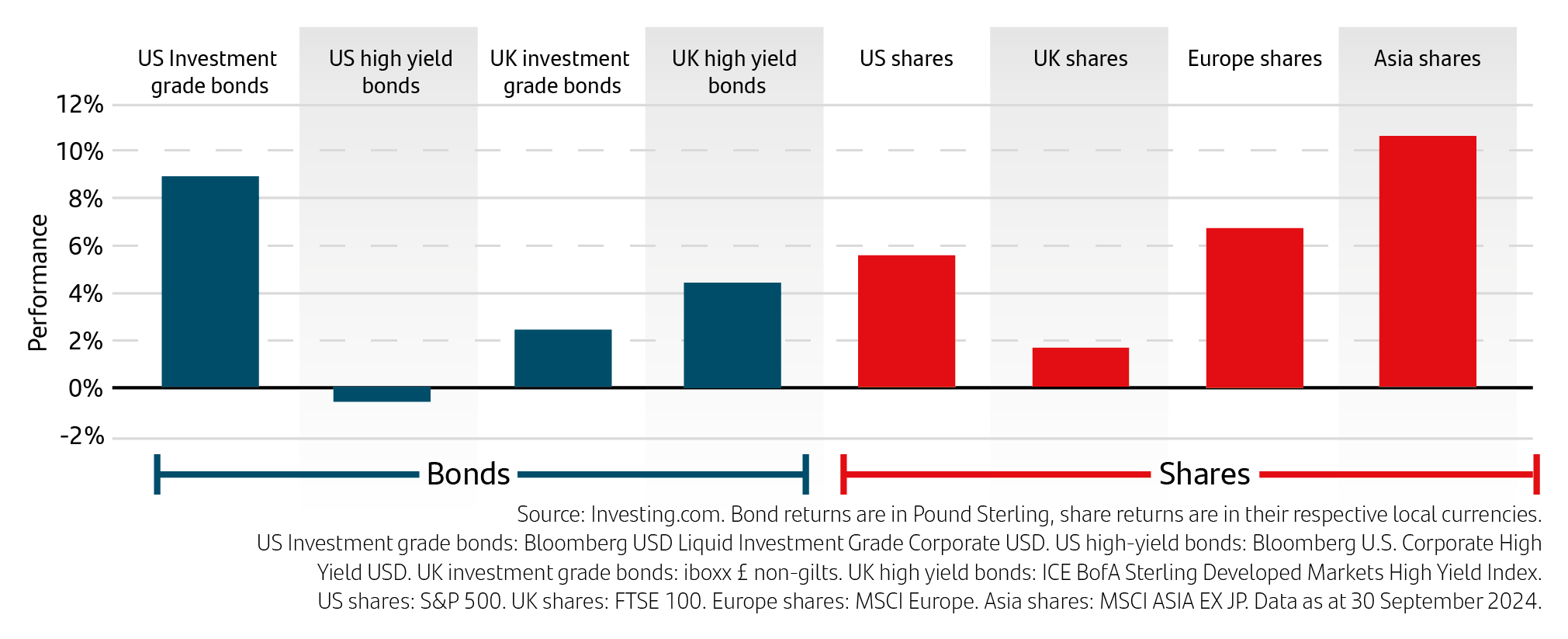

The upward trend in global stock markets continued during the third quarter, supported by long anticipated interest rate cuts from the major global central banks. While returns were reasonable in US dollar and local currency terms, the pound’s strength meant that in sterling terms they were minimal.

Emerging markets outperformed developed world markets, largely due to the Chinese market’s surge towards the end of the period, which resulted from a raft of new stimulus measures. Among the larger developed markets, the US again led the way, outperforming Europe, the UK and Japan in local currency terms.

Each of the BoE,1 the ECB2 and the US Fed3 cut rates during the period, as expected, with the Fed cutting by more than the other central banks. Falling inflation across most countries and central banks’ gradual acceptance that the current disinflationary trends were likely to be persistent led them to cut rates, with further easing expected before the end of the year. Meanwhile, the Bank of Japan (BoJ)4 danced to a different tune and raised rates for the second time this cycle in July, following March’s hike.

Many major market indices continued to set new all-time highs during the period.5 This was driven not only by falling interest rates, but by hopes that the US economy would achieve a soft landing, and resilient corporate earnings. Geopolitical tensions, especially those in the Middle East, caused volatility but did not ultimately derail the positive sentiment towards equities.

Economic data was largely mixed. Despite signs of a slowdown, especially in its labour market, the US continued to lead developed market growth, with GDP rising by 3.0%6 in the second quarter of the year (on an annualised basis). Recent economic data emanating from the eurozone and UK , including monthly GDP7 and retail sales,8 underlined the fragile nature of their respective economies. China’s second-quarter GDP disappointed expectations,9 as slowing industrial production growth10 and its problematic housing and commercial property sectors weighed on growth. India continued to grow strongly although there were increasing signs of a slowdown.11

Bond markets also produced positive returns, supported by falling inflation and rate cuts. Against this background, higher-risk corporate bonds performed better than government bonds.

3rd quarter asset class performance

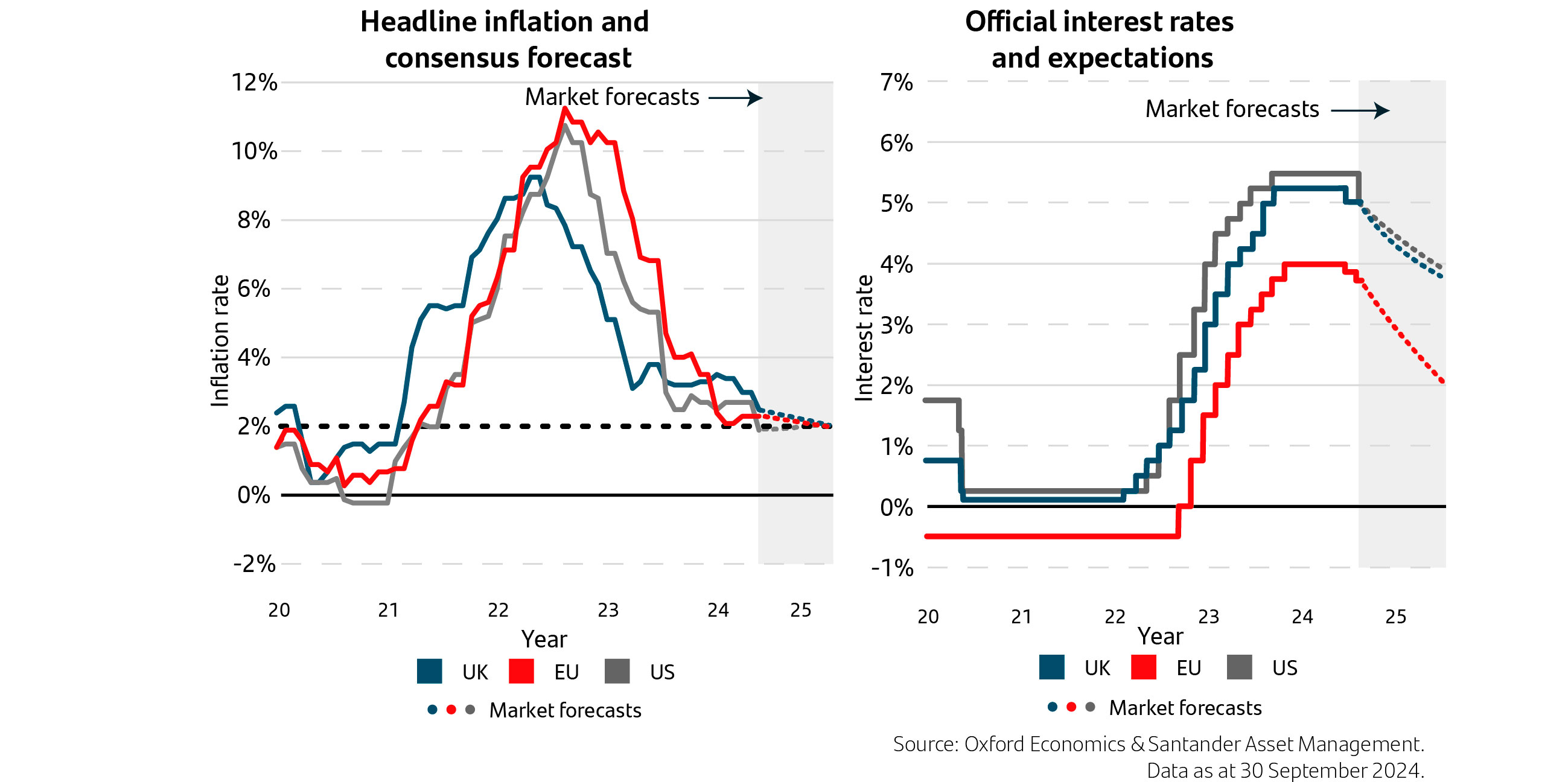

Inflation and interest rates

Inflation and interest rates have been dominating the financial news lately, and for good reason. Understanding these measures is crucial to making informed investment decisions, as they can help explain why your portfolio may be behaving in a certain way. The two charts below provide a view of historic and current trends in these areas, helping you to better understand what’s going on in the current economy.

When interest rates go up, it becomes more expensive to borrow money, which can lead to a decrease in consumer spending and economic growth. This can cause shares and bonds to lose value and make it harder for companies to generate profits, which can ultimately hurt investment returns.

When interest rates go up, it becomes more expensive to borrow money, which can lead to a decrease in consumer spending and economic growth. This can cause shares and bonds to lose value and make it harder for companies to generate profits, which can ultimately hurt investment returns.

However, rising interest rates can be a powerful tool for tackling inflation. The slowdown in spending helps to reduce the upward pressure on prices that contributes to inflation. While rising interest rates may have a negative impact, it can play an important role in keeping inflation in balance.

Inflation and interest rates outlook

Expectations for interest rate cuts in the UK have ramped up after the Governor of the BoE said UK policymakers could become a ‘bit more aggressive’ in their approach if inflation continues to cool. The next Monetary Policy Committee (MPC) meeting is set to take place on 7 November.12 However, even with inflation being close to the BoE’s target of 2%, we think that they will be cautious in their approach of bringing rates down and believe that a cut of 0.25% is more likely in November. Rates could be cut by a further 0.25% in December, but this would depend on the economic data releases leading up to the MPC meeting.

The Fed cut its benchmark interest rate by a sizable 0.50% at its September meeting, the first cut in more than four years. There were some fears amongst the market that the US could be heading towards an economic downturn, however, jobs data released in early October thwarted these fears and painted a rosier picture of the economy. The strong US job market data along with other strong economic data points is likely to halt the likelihood of a future 0.50% cut by the Fed. We think a 0.25% cut is most likely in November followed by a further 0.25% cut in December.

Share outlook

The market has been particularly volatile during this quarter and has served as a reminder that sentiment can move markets, yet company fundamentals prevail in the end.

The final quarter of the year brings some key issues for investors to contemplate, which could cause some further market turbulence. While volatility may sound bad, it’s important to remember that it involves ups as well as downs. The US election is due in November and while history shows that the winning candidate or party has little long-term bearing on market returns, it is also interesting to note that markets do tend to have a reaction (either positive or negative) on election outcomes. Elections may have short-term market impact, but the change in political regime tends to have little sway over longer-run share performance.

Also likely to influence market sentiment in the fourth quarterare Fed rhetoric and rate cuts. Shares generally perform well on Fed easing, particularly when rate cuts are not accompanied by a recession.

Shares have been on a positive streak for around a year, so it wouldn’t be surprising to see some form of market correction. However, we think that there is still room to run before this could happen.

Bond outlook

Currently, our strategy is to increase exposure to riskier assets, such as shares, and move away from safer assets like developed market bonds and cash.

Our strategy is driven by three key events from the past month. Recent US jobs data in the US has showed that there could be some improved momentum in economic growth than what was originally thought, reducing the likelihood of a recession, and providing great clarity on the outlook for the future . The Fed has also initiated a cycle of rate cuts, and sentiment in China has improved following stimulus measures by the People’s Bank of China, aimed at stabilising the real estate market and supporting share prices. These three key events should create a more attractive scenario for shares over bonds.

We are currently in favour of slightly riskier bonds, such as investment grade and high yield bonds, as they are currently offering attractive return for the associated risk when compared to government bonds.

Baffled by bonds?

Visit our Basics on Bonds page for more information.

Our tactical asset allocation

Our tactical asset allocation represents our views on the financial markets based on the current market conditions and our own market outlook over the coming months. The below chart demonstrates how our current positioning is either underweight, overweight or neutral when compared to a funds benchmark. Generally, an underweight position means that we think a sector will perform worse than others, so we hold less of it. Holding an overweight position means that we think a sector will perform better, so we hold more of it. A neutral position means that we think a sector will perform similarly to others, so we will hold a similar amount as the benchmark.

Summary

- The upward trend in global stock markets continued during the third quarter, supported by long-anticipated interest-rate cuts.

- The strong US job market data along with other strong economic data points is likely to halt the likelihood of another 0.50% cut by the Fed.

- The US election could cause some short-term market turbulence.

- Shares have performed well so far this year and we have a positive view on shares going forward.

- We are happy to take on additional risk within our funds and are therefore overweight shares relative to bonds.

Learn more, visit our website here for more insights into financial markets.

Note: Data as at 21 October 2024. 1Bank of England, 1 August 2024. 2CNBC, 12 September 2024. 3CNBC, 18 September 2024. 4Financial Times, 31 July 2024. 5Reuters, 26 September, 2024. 6Associated Press News, 26 September 2024. 7Reuters, 11 September 2024. 8Trading Economics, 30 September 2024. 9Associated Press News, 15 July 2024.10Trading Economics, 30 September 2024.11Reuters, 30 August 2024.12Sky news, 3 October 2024.

Important information

For retail distribution.

This document has been approved and issued by Santander Asset Management UK Limited.

This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities or other financial instruments, or to provide investment advice or services. Opinions expressed within this document, if any, are current opinions as of the date stated and do not constitute investment or any other advice; the views are subject to change and do not necessarily reflect the views of Santander Asset Management as a whole or any part thereof. While we try and take every care over the information in this document, we cannot accept any responsibility for mistakes and missing information that may be presented.

The value of investments and any income is not guaranteed and can go down as well as up and may be affected by exchange rate fluctuations. This means that an investor may not get back the amount invested. Past performance is not a guide to future performance.

All information is sourced, issued and approved by Santander Asset Management UK Limited (Company Registration No. SC106669). Registered in Scotland at 287 St Vincent Street, Glasgow G2 5NB, United Kingdom. Authorised and regulated by the Financial Conduct Authority (FCA). FCA registered number 122491. You can check this on the Financial Services Register by visiting the FCA’s websitewww.fca.org.uk/register.

Santander and the flame logo are registered trademarks. www.santanderassetmanagement.co.uk