Q2 2023

This publication aims to provide an insight into the changing economic environment and importantly, how this has impacted financial markets and investments. Our Multi-Asset Solutions team at Santander Asset Management UK share their thoughts on the market outlook and how they have adapted investment portfolios to position our clients for the road ahead.

Summary of Quarterly Perspectives content:

- Review of second quarter of 2023

- Investment performance of different asset classes year to date

- Our expert’s opinion on the investment outlook

- How have our fund managers changed their portfolio positioning based on the outlook and our tactical asset allocation

- Summary of the quarterly perspectives

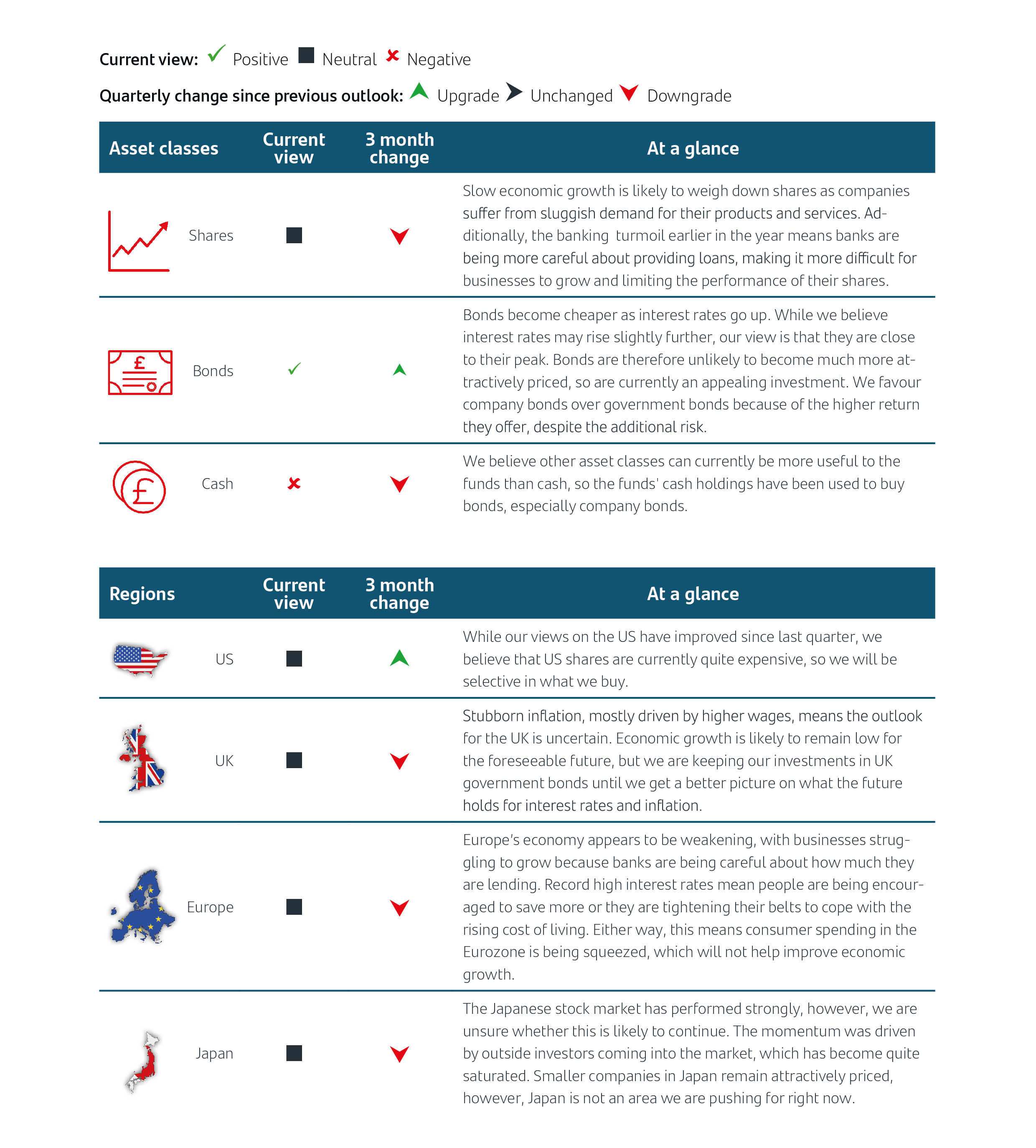

Outlook at a glance Reviewing the second quarter of the year

Reviewing the second quarter of the year

It was a positive quarter for the majority of global stock markets after a slowdown in US inflation gave investors hope that the Federal Reserve (Fed) would stop raising interest rates. Stock markets were also helped by growing interest in Artificial Intelligence (AI), which saw technology sector shares recover some of the ground they lost during last year’s market downturn.1

The S&P 500 Index, which tracks the largest companies listed on the New York Stock Exchange, experienced its biggest quarterly gain since the end of 2021. The Nasdaq Composite Index, which includes a significant number of technology companies, rose sharply as firms involved in AI received more investor attention and interest. The Nasdaq has now experienced back-to-back quarters of growth.2

Despite the strong stock market performance, economic signals are mixed. A report released in late June found that consumer spending was still low in May, but other data revealing strong new home sales and durable goods (goods not for immediate consumption and able to be kept for a period of time) orders suggested the economy was stronger.3 On 30 June, the final day of the quarter, the US Supreme Court blocked a plan to erase $430 billion of student debt, a move that could have put a lot of money back into the pockets of former students and boosted consumer spending.4

The Fed raised interest rates for the tenth time in a row at its May meeting, before pausing in June5 so it can assess the impact of the earlier rate hikes.6 This does not necessarily mean interest rates will start to come down, however, as the US central bank believes more increases may be necessary.

In the UK, efforts to bring inflation down have been less successful and it was higher than expected every month from February to May. There was also an unexpected jump in core inflation, which strips out prices items such as food and energy as they can be more volatile.7

In May, the Bank of England (BoE) opted for a relatively small increase to its interest rate, but the disappointing inflation figures triggered a larger-than-expected hike in June.8

Stubbornly high inflation and weak economic growth are not good news for UK shares. The two main stock markets for the UK are the FTSE 100 Index and the FTSE 250 Index. The FTSE 100 is made up of mostly large companies that earn the majority of their income from abroad, so they benefit when the pound is weaker as they profit from converting currency from overseas. Over the quarter, the pound made positive gains against the US dollar, which in turn negatively affected the FTSE 100’s performance. The FTSE 250 is mostly made up of UK companies selling into the UK. Both ended Q2 lower than where they started, ending back-to-back quarters of gains.9

The European Central Bank (ECB) has made clear that the battle against inflation in the Eurozone is far from over, even though the euro area annual inflation rate is down from a peak of 10.6% in October to 6.1% in May 2023. Its target is 2%.10

The ECB raised interest rates twice during the quarter. It now expects core inflation to remain higher this year than forecast, with rising wages and slow growth the main culprits behind the worsening outlook.11

Figures released in June showed that the Eurozone slipped into a mild recession in the first quarter, as higher living costs made consumers think twice before spending and they were incentivised to save money instead. A recession is defined as two consecutive quarters of negative growth.12

European shares rose during the quarter, fuelled by hopes that Chinese authorities will look to revive China’s faltering economy by pumping in more money. A healthier Chinese economy is good news for European shares as China is a major buyer of European luxury brands.13 However, due to weak Chinese demand and worries about more interest rate hikes, the Q2 uplift in share prices was not as strong as the one recorded earlier this year.14

Japan’s Nikkei 225 Index, which tracks the 225 largest companies listed on the Tokyo Stock Exchange, rose for a third quarter in a row and recorded its largest quarterly gain since the end of 2020.15

In April, billionaire investor Warren Buffett said he was optimistic about Japanese shares after broadening his investments in the country.16 Demand from foreign investors is being driven by better-than-expected company earnings, reforms by the Tokyo Stock Exchange and a weak yen – which made Japanese exports cheaper, so more competitive.17

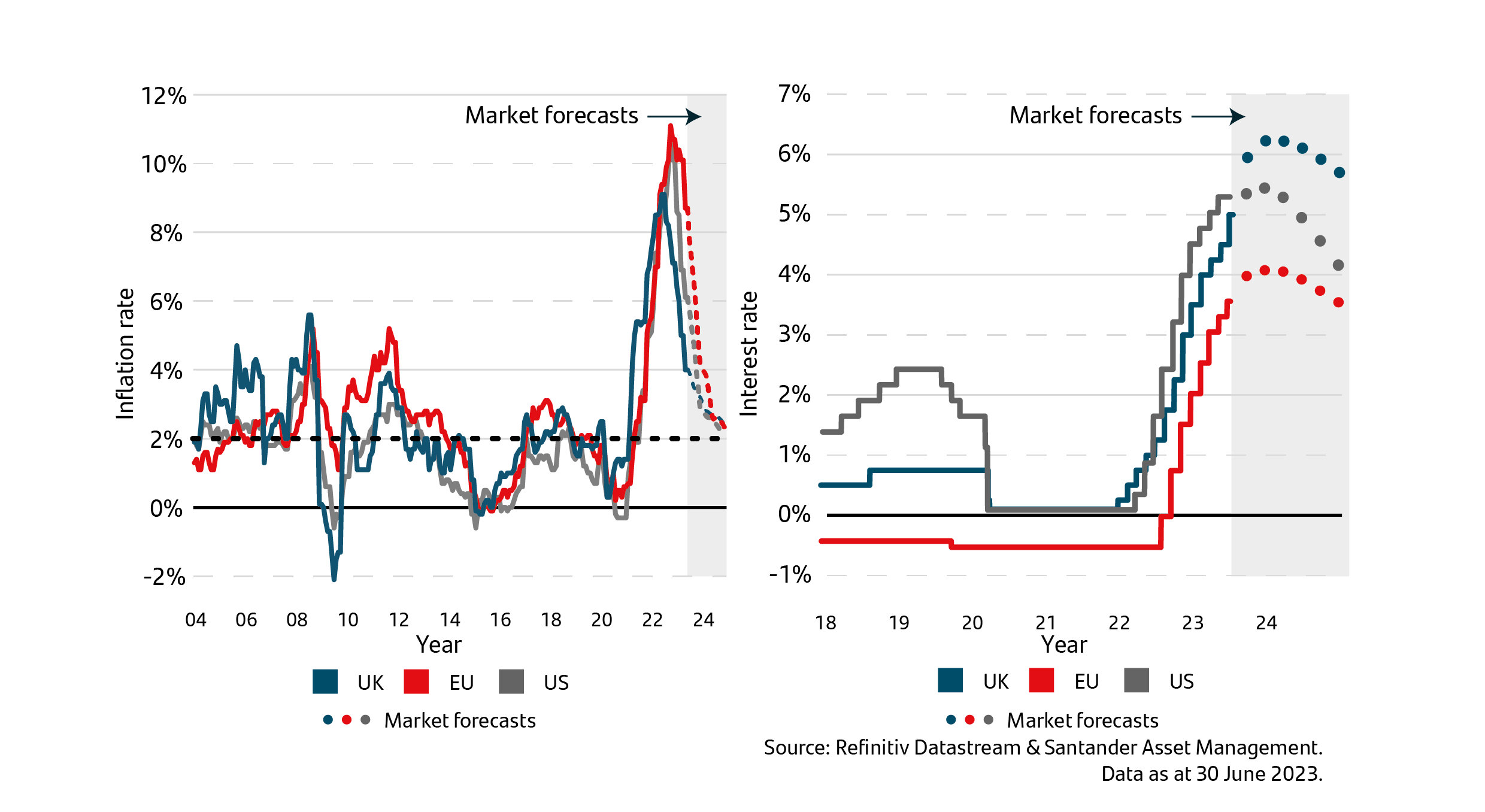

2nd quarter asset class performance Inflation and interest rates

Inflation and interest rates

Inflation and interest rates have been dominating the financial news lately, and for good reason. Understanding these measures is crucial to making informed investment decisions, as they can help explain why your portfolio may be behaving in a certain way. The two charts below provide a view of historic and current trends in these areas, helping you to better understand what’s going on in the current economy.

Left: Headline inflation and consensus forecast. Right: Official interest rates and expectations

When interest rates go up, it becomes more expensive to borrow money, which can lead to a decrease in consumer spending and economic growth. This can cause shares and bonds to lose value and make it harder for companies to generate profits, which can ultimately hurt your investment returns. However, rising interest rates can be a powerful tool for tackling inflation. The slowdown in spending helps to reduce the upward pressure on prices that contributes to inflation. While rising interest rates may have a negative impact, it can play an important role in keeping inflation in balance.

Inflation and interest rates outlook

We believe inflation will probably slow by the end of the year, helped by lower energy bills and food prices, but it may take longer to fall to the 2% targets set by the Fed, ECB and the BoE. This is because they face a challenging balancing act of raising interest rates to fight inflation, without raising them to the point where consumers stop spending and start to damage economic growth. Low unemployment in Europe, the UK and the US, coupled with strong wage growth, means consumer spending is still high when compared to historic levels, even though consumers are starting to spend less. This is a double-edged sword, making it easier for economies to grow but this also fuels inflation, meaning that interest rates may have to stay higher for longer.

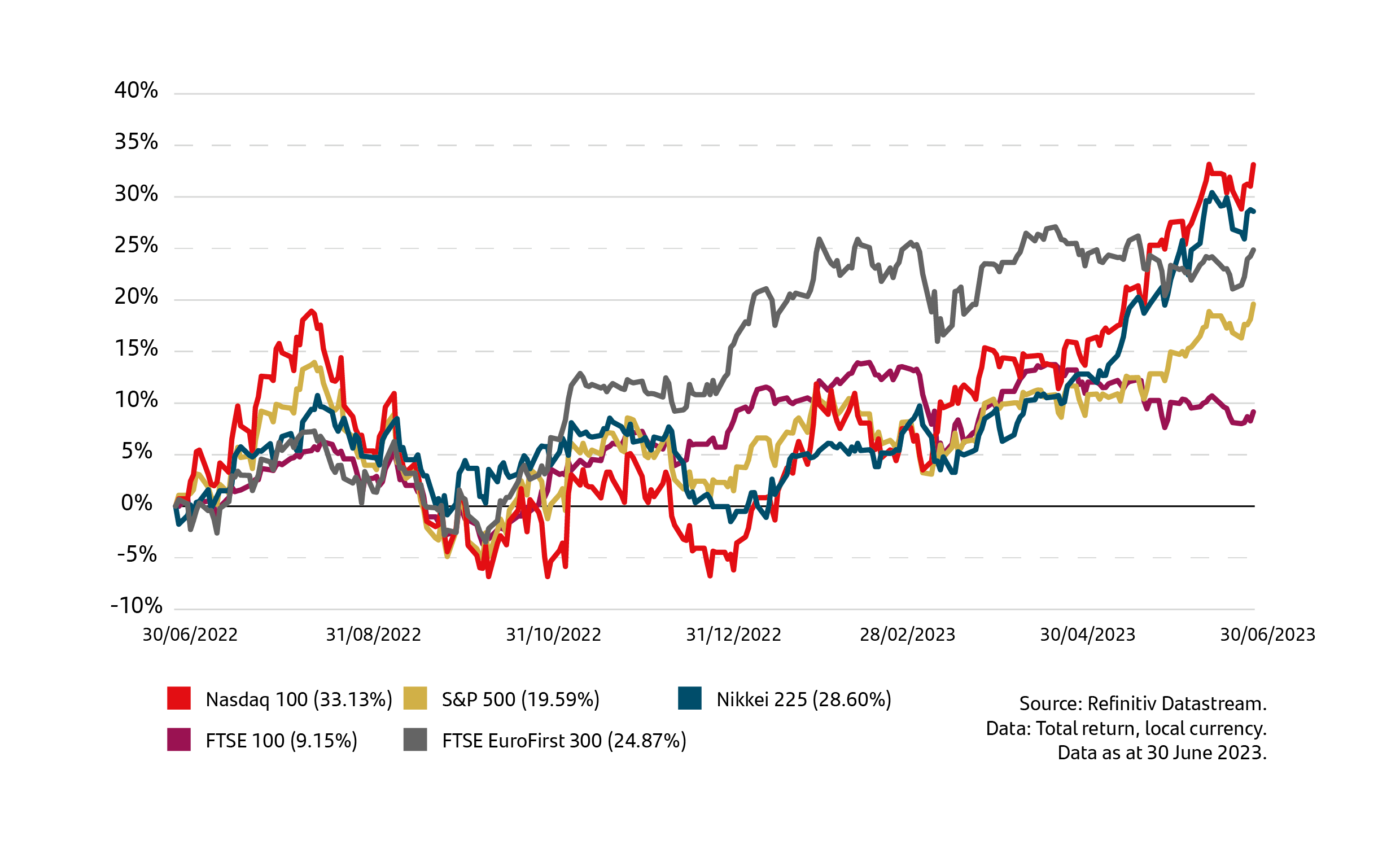

Shares

The below chart demonstrates how various indexes have performed over the last year. An index is a collection of stocks that are grouped together to represent the overall performance of a particular market or sector. In this case, we’re looking at major indices from different regions around the world, such as the S&P 500 in the United States, the Nikkei 225 in Japan, the FTSE EuroFirst 300 in Europe, the FTSE 100 in the United Kingdom and the NASDAQ 100 which includes 100 of the worlds largest non-financial companies. These indices are made up of the largest and most influential companies within a given market, and their performance can give us an idea of how well that particular economy is doing.

Share index performance

Share outlook

During the second quarter, we modified our portfolios from owning more shares than the benchmark to a more neutral position where we hold a comparable number of shares. Shares had performed strongly from the start of the year, especially US shares, pushing up prices to a point where we felt the impact of rising interest rates combined with the fallout from the banking crisis would impact shares in the short term. Higher borrowing costs, along with a more cautious approach from banks towards lending, will stifle growth and dampen stock markets, in our view. While stock markets continued to perform well throughout the second quarter, the impact of higher interest rates, tighter lending conditions for business and slowing consumer demand may not necessarily lead to a recession, especially in the US, but we believe these are significant headwinds that justify our neutral position.

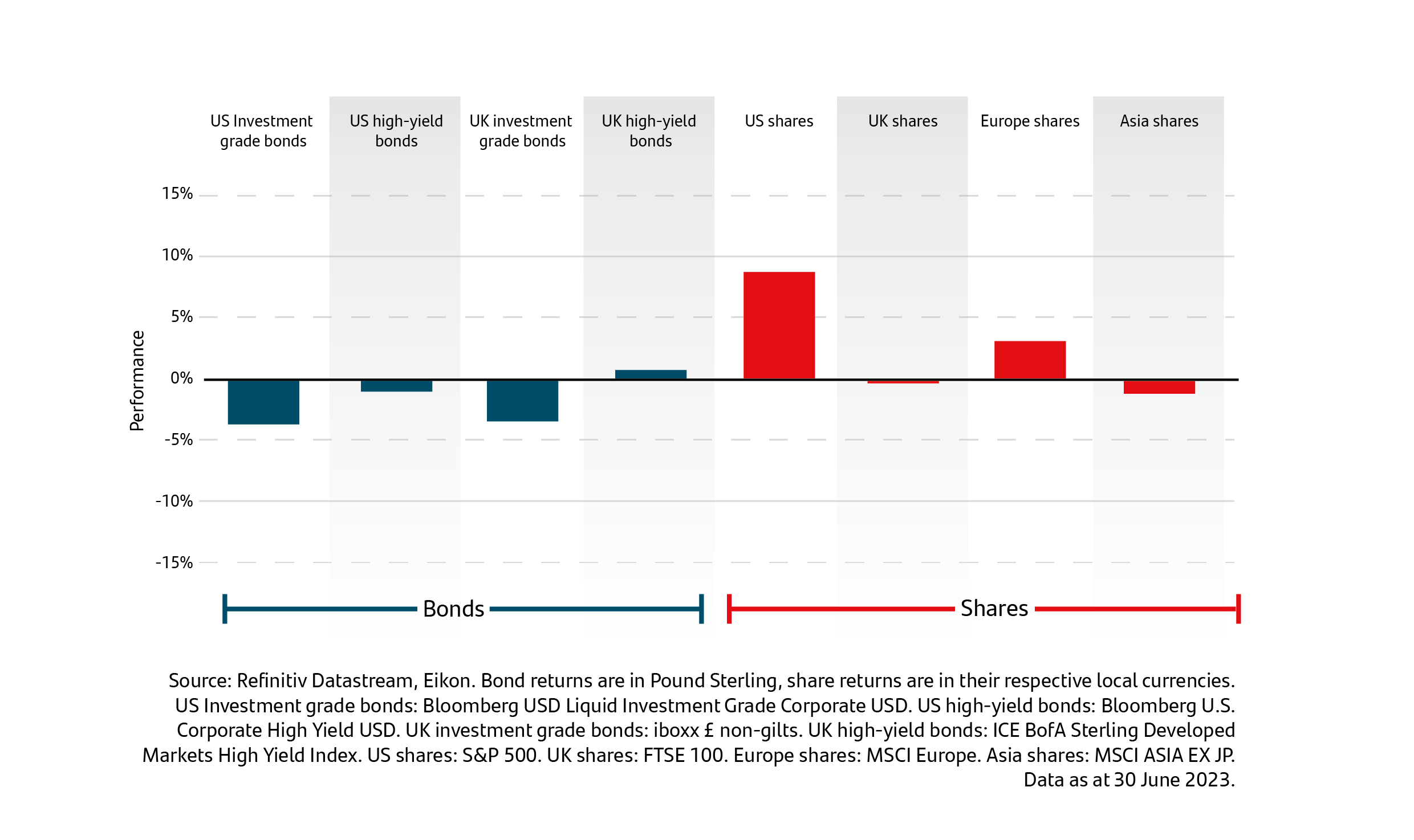

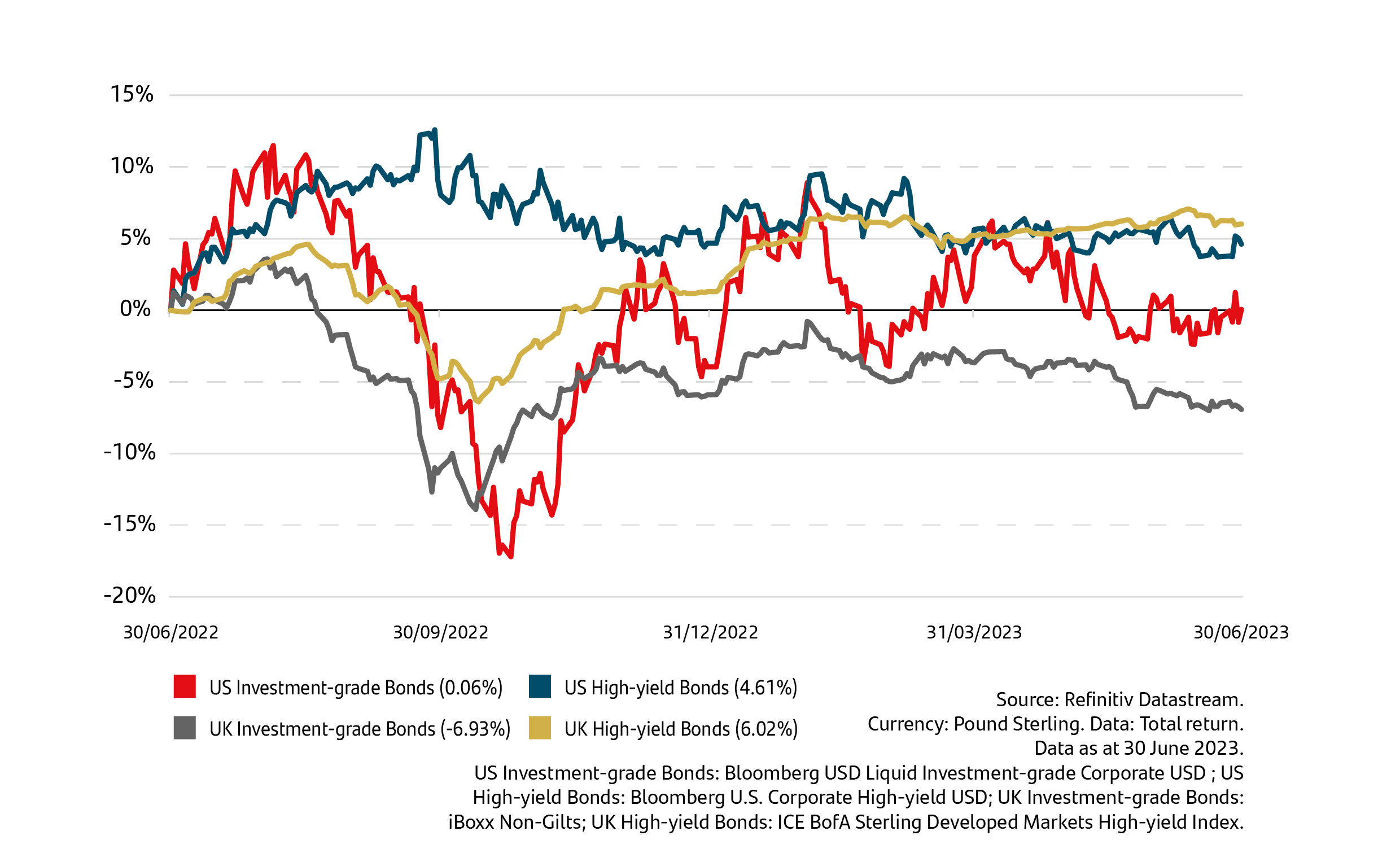

Bonds

The chart below demonstrates how global bond indexes have performed in the past year. Bond indexes track the performance of a group of bonds and are typically created by selecting a specific set of bonds that meet certain criteria, such as maturity dates, credit ratings, or other characteristics. There are many different types of bond indexes, including those that track government bonds, corporate bonds, municipal bonds, or bonds from a particular region or country. Just like equity indexes, bond indexes provide investors with a convenient way to track the performance of a particular segment of the market.

Bond index performance

Investment-grade bonds: Issued by companies considered most financially secure and least likely to default on their loans.

High-yield bonds: Issued by less stable organisations, with a higher rate of interest to compensate for the higher chance of defaulting.

Bond outlook

Bonds have become a much more attractive investment over the last couple of years. Rising interest rates in response to inflation have seen bond yields rise in line with higher rates, and as a result, bond values have fallen significantly, meaning that bonds are now priced at attractive prices with high yields. Towards the end of the second quarter, we started to move more of the cash held in portfolios into bonds to take advantage of lower valuations and higher yields. While inflation has been slower to fall than initially forecast, meaning interest rates are likely to stay higher for longer, our conviction remains that we are very near the peak of interest rates. Our view is that it may be some time before central banks begin to consider cutting rates in the future, even in the event of a significant economic slowdown. However, investment markets tend to anticipate the future path of interest rates, which is then reflected in the change in both yields and values. Our preference is for company bonds over government bonds, as they offer higher yields despite the moderate additional risk. The funds are running low on cash as we have been using some of their cash reserves to buy more bonds.

Baffled by bonds?

It may be worth taking some time to learn the basics to help you better understand how they work.

Visit our Basics on Bonds page for more information.

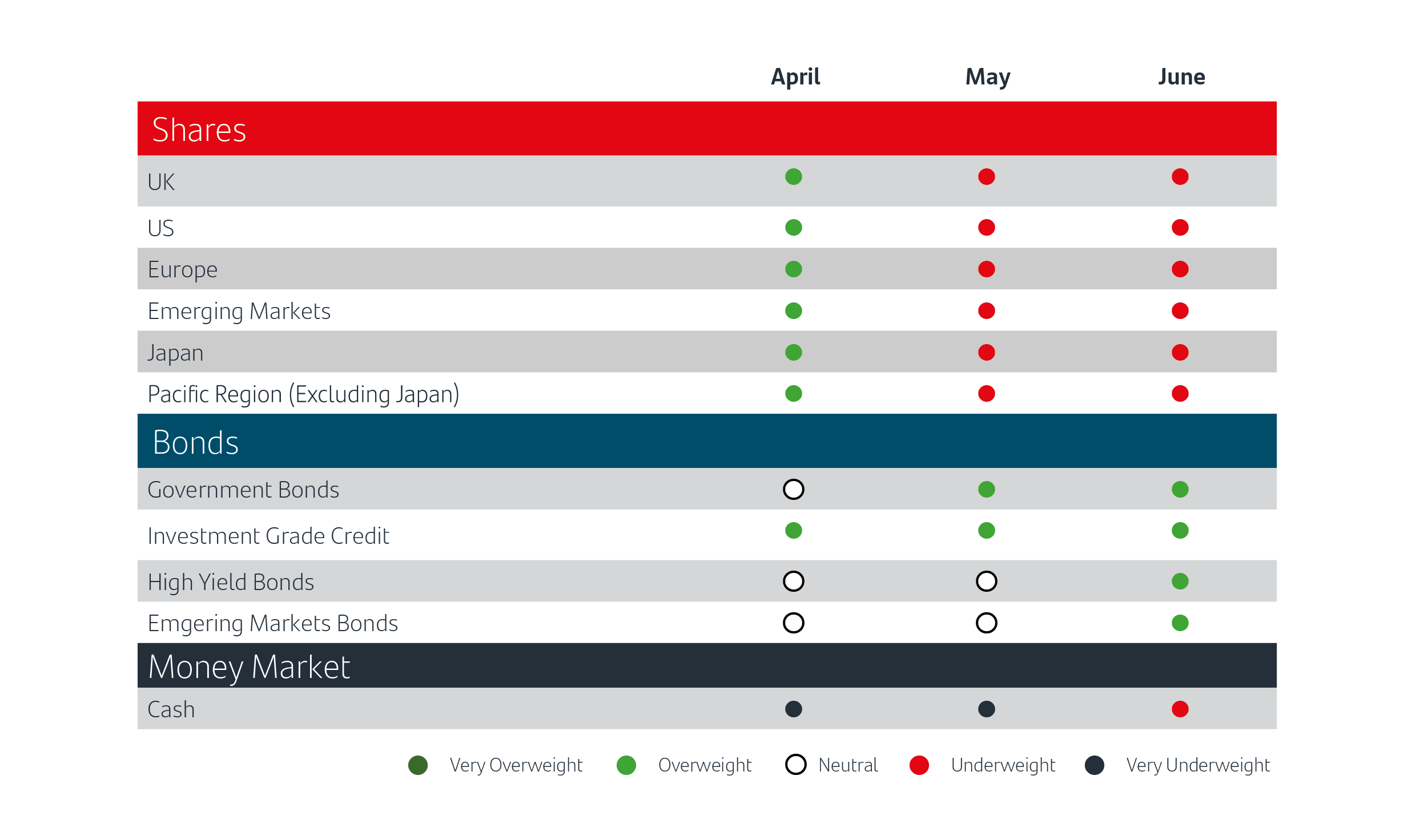

Our tactical asset allocation

Our tactical asset allocation represents our views on the financial markets based on the current market conditions and our own market outlook over the coming months. The below chart demonstrates how our current positioning is either underweight, overweight or neutral when compared to a funds benchmark. Generally, an underweight position means that we think a sector will perform worse than others, so we hold less of it. Holding an overweight position means that we think a sector will perform better, so we hold more of it. A Neutral position means that we think a sector will perform similarly to others, so we will hold a similar amount as the benchmark.

Summary

- The second quarter of 2023 saw the return of the traditional relationship between bond and stock markets, with shares rising in value while bonds fell, helping smooth the investment journey for our multi-asset solutions.

- The banking turmoil in March was brought under control by regulators, but its effects were still being felt in Q2 as banks became more reluctant to lend, meaning businesses found it harder to borrow money and grow, which weighed down stock market performance.

- Despite these difficulties, many economies, including the US and UK, were stronger than expected and many stock markets produced positive returns during the quarter.

- Financial results from companies showed a better Q1 (January to March 2023) than was expected, which is another positive sign for investors that the underlying economies are strong.

- Bond prices have generally fallen this quarter, with increases in interest rates resulting in elevated bond yields and therefore lower prices.

- We have reduced our stance on shares to neutral to reflect higher prices and a more challenging outlook.

- We have increased our positioning in bonds to overweight across portfolios as bond yields have risen and values have fallen.

- Given that interest rates appear to be nearing their peak, our view is that bond prices are unlikely to fall much further.

Investing can feel complex and overwhelming, but our educational insights can help you cut through the noise. Learn more about the Principles of Investing here.

Data as at 30 June 2023. 1Reuters, 30 June 2023. 2CNBC, 30 June 2023. 3Bloomberg, 30 June 2023. 4Reuters, 30 June 2023. 5Federal Reserve, 14 June 2023. 6CNBC, 14 June 2023. 7Bloomberg, 21 June 2023. 8Reuters, 22 June 2023. 9Reuters, 30 June 2023. 10Associated Press, 27 June 2023. 11CNBC, 15 June 2023. 12The Guardian, 8 June 2023. 13Jing Daily, 4 May 2023. 14Reuters, 30 June 2023. 15Dow Jones, 30 June 2023. 16CNBC, 5 May 2023. 17CNBC, 26 June 2023.

Important information

For retail distribution.

This document has been approved and issued by Santander Asset Management UK Limited.

This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities or other financial instruments, or to provide investment advice or services. Opinions expressed within this document, if any, are current opinions as of the date stated and do not constitute investment or any other advice; the views are subject to change and do not necessarily reflect the views of Santander Asset Management as a whole or any part thereof. While we try and take every care over the information in this document, we cannot accept any responsibility for mistakes and missing information that may be presented.

The value of investments and any income is not guaranteed and can go down as well as up and may be affected by exchange rate fluctuations. This means that an investor may not get back the amount invested. Past performance is not a guide to future performance.

All information is sourced, issued and approved by Santander Asset Management UK Limited (Company Registration No. SC106669). Registered in Scotland at 287 St Vincent Street, Glasgow G2 5NB, United Kingdom. Authorised and regulated by the Financial Conduct Authority (FCA). FCA registered number 122491. You can check this on the Financial Services Register by visiting the FCA’s websitewww.fca.org.uk/register.

Santander and the flame logo are registered trademarks. www.santanderassetmanagement.co.uk